How Your Marijuana Use Affects Your Chances Of Getting Approved And Securing The Best Rates For Life Insurance In 2025

Want to hear a little-known fact?

George Washington grew marijuana in his farm (supposedly to deal with his toothaches).

Here’s another.

In Colorado, medical marijuana dispensaries currently outnumber Starbucks locations three to one.

Shocking right?

Americans love to smoke or use marijuana in some way, shape or form. But that should come as no surprise.

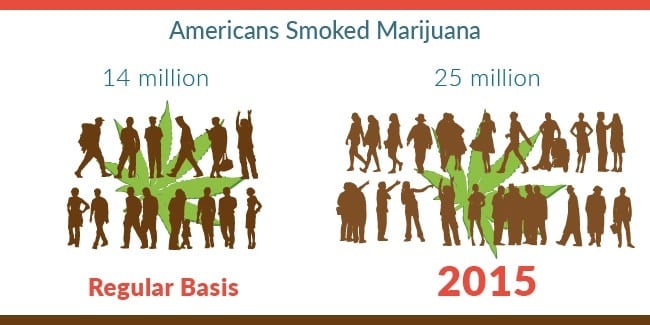

According to new research, around 25 million Americans have used marijuana in the past year.

And as of Jan. 2025, many states have approved marijuana for either recreational or medical initiatives.

With an increasing number of states legalizing marijuana for medical or recreational use, many marijuana users are seeking life insurance to help protect their families and investments should anything unfortunate happen to them before their time.

In the past, life insurance companies often denied marijuana users any coverage. And when people tried to increase their coverage after medical tests revealed marijuana use, some policies were canceled altogether.

Today, the life insurance landscape has changed, and the industry has lightened up on marijuana use over the past two decades.

In fact:

Sun Life and BMO Insurance are the first two major Canadian insurance companies that have decided to treat marijuana users as non-smokers and reverse long-standing policies that assessed users of marijuana as being “high-risk” and on an equal level with tobacco smokers.

University student Jonathan Zaid was recently successful in getting Sun Life to treat all medical marijuana users as non-smokers.

The decision means users of marijuana and cannabis for medical and recreational reasons can receive cheaper premiums and Jonathan now has his medical marijuana expenses covered by his insurance plan.

So how does the ol’ Mary Jane affect your ability to secure a life insurance policy if you’re a recreational or medicinal marijuana user, especially if you are an American?

Let me first give you the lowdown on some common concerns surrounding life insurance and marijuana:

- Yes, you can get approved for life insurance even if you smoke or use marijuana.

But there are additional things to consider when compared with those who don’t use marijuana. The main issue for underwriters is tetrahydrocannabinol, also known as THC.THC is a chemical compound found inside the marijuana plant, which is responsible for bringing on the euphoric high.If a lab test reveals the presence of THC in your blood, some insurers may consider you a cigarette smoker, which means you could pay expensive smoker rates and higher premiums. Another issue is that some insurers may deem you as a smoker regardless of how often you use marijuana.

If you have a prescription for medical marijuana, you could still qualify for the best life insurance rates but insurance companies will want to know what condition the marijuana is prescribed to treat and why. If you’re a recreational pot user, you can also qualify for life insurance but most likely at standard rates. It depends largely on how often you smoke or use the drug. The key is to find a company that considers you a non-smoker.

- Life insurance companies will often test for drugs and these tests can detect THC.

Insurance companies do carry out blood and urine tests and sometimes do mouth swabs to check the overall health of the applicant. These tests can detect the presence of illegal drugs such as THC. Testing positive for THC doesn’t mean you’ll get rejected for a life insurance policy, however, the use of this substance can result in you being asked to pay a tobacco smoker’s rate, which is more expensive than non-smoker rates.

That said, there are policies available that do not require you to undertake a medical exam. These are mainly for term life insurance only, and you can expect to pay higher premiums for these.

- A marijuana prescription can make it more expensive to get life insurance.

If your prescription is for a condition that doesn’t normally affect your rates, you’re better off than the casual marijuana smoker. But if it’s for something significant, you’ll be rated based on the normal risks associated with that condition or disease.

- If you use marijuana, don’t lie about it

The best approach to getting a good deal on your life insurance is, to be honest about your marijuana use. Find a good independent agent who knows what they’re doing and can help you apply to a company that’s more marijuana-friendly.

Choosing the wrong life insurance company can result in your application being denied or you might get lumped in with cigarette smokers, which means you could end up paying expensive smoker rates.

That’s why we created this guide.

Today, we explore everything you need to know about getting the best rates for life insurance if you use marijuana, including tips on how to increase your chances of getting approved, how to avoid choosing the wrong company, and the top marijuana-friendly life insurance companies you should look at.

1. Marijuana is the World’s Third Most Popular Recreational Drug

Marijuana use goes back to 6000 BC when cannabis seeds were used for food in China.

Today, marijuana is the third most popular recreational drug in the world (behind only alcohol and tobacco).

And has been used by nearly 100 million Americans, according to NORML an organization working to legalize marijuana.

Government surveys reveal that approximately 25 million Americans have smoked marijuana in the past year and more than 14 million do so on a regular basis.

That’s a lot of Americans smoking marijuana.

A study published in the journal JAMA Psychiatry revealed that marijuana use in America has doubled in the past decade, while marijuana abuse has decreased since 2002.

The most significant increases in marijuana are among Americans aged 45-64, as well as in African American and Native American populations.

Seven percent of adult Americans say they smoke marijuana, with the average regular user smoking 2-4 joints each day.

While 38% of Americans admit to having tried marijuana, it’s adults in the 18 to 29 age bracket who are the heaviest users today.

2. Legalized Marijuana is the Fastest-Growing Industry in America (and the Government Loves It)

Marijuana is a $5.7 billion market.

And sales of recreational marijuana could surpass medical marijuana as early as 2018, according to a new report from Marijuana Business Daily.

Last year, the marijuana market in the US was bigger than that for craft beer, wine and organic food.

To put this in perspective, legal cannabis outsold Girl Scout cookies in 2015.

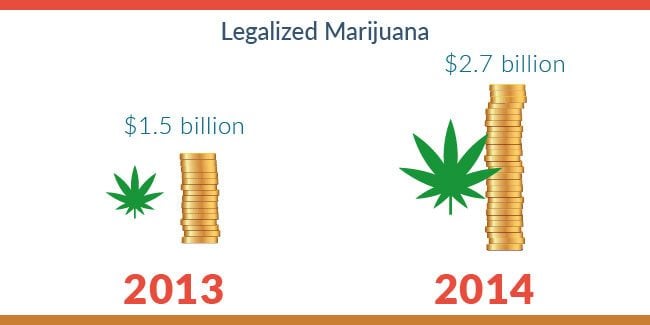

According to cannabis industry investment and research firm, The ArcView Group, legalized marijuana is the fastest-growing industry in America, up from $1.5 billion in 2013 to $2.7 billion in 2014.

With ArcView predicting that medical and recreational marijuana sales will surpass $22 billion by 2020, it’s easy to see why the government loves it.

In the first 18 months after the drug was legalized in Colorado, and later in Washington State, tax revenue on cannabis topped $200 million.

And it’s not only the public sector reaping the benefits of the marijuana market.

The growing marijuana market could mean big business for Silicon Valley entrepreneurs with one investor, who typically backs mainstream startups like Flywheel, steering $200,000 to Tradiv, an online marketplace for wholesale cannabis.

Even Microsoft Corp. recently announced a partnership to track marijuana for local and state governments.

Marijuana is now legal in some form in over half the states in the US, with a total of 28 states, plus the District of Columbia, now allowing the medical use of marijuana.

The official number of medical marijuana patients holding identification cards in the US (and District of Columbia) is over 1.2 million.

On November 8 2016, another four states voted in favor of outright marijuana legalization. California, Nevada, Maine, and Massachusetts all voted in favor of legalized use, sale, and consumption of recreational marijuana.

That means eight states have now approved to legally tax and regulate marijuana (Alaska, California, Colorado, Maine, Massachusetts, Nevada, Oregon and Washington) while 20 states have decriminalized marijuana by eliminating criminal penalties for simple possession of small amounts for personal use.

With four states voting to legalize marijuana for recreational use, and four states, including Florida, North Dakota, Arkansas and Montana, voting to approve marijuana for medical use at the November 8 ballot, you can expect these numbers to increase over the next few years.

In the states with outright legalization, the possession and consumption of marijuana is legal for people aged 21 and older.

With 58% of Americans in favor of legalization, the question is not if but when it will be legal in all 50 states…which leads us on to our next point.

3. A Majority of the Country Supports Marijuana Legalization

Support for marijuana legalization has steadily increased over the past 25 years.

In 1990, just 16% of those surveyed by CNN/ORC supported legalizing the drug. That figure is now at 58%, according to the most recent Gallup poll.

This is the highest percentage support ever reported in a nationwide scientific poll.

Eight out of ten Americans support the medical use of marijuana and nearly three out of four Americans support a fine-only penalty for recreational smokers.

This is a clear sign that as marijuana becomes legal in more states, support for greater access to marijuana also increases.

Meet Tom, the one of a kind farmer whose plan is to educate the public on everything marijuana

Tom Lauerman is a medical marijuana farmer and owner of Farmer Tom’s Collective. He lives in Vancouver in Washington State and owns the only federally approved medical cannabis farm in the US.

Tom has dedicated his life to normalizing cannabis and he’s on a mission to legalize medical marijuana across the United States. His dream is to one day have farmers everywhere be able to use his brand and market to their benefit.

After a car crash in the 1990s, Tom was left with severe back injuries and swears by marijuana’s medicinal properties. Despite being arrested in 1999 at his medical collective for using marijuana, he’s now working with the federal government and authorities to establish the first ever national safety guidelines for the cannabis industry.

Here’s an awesome video about Tom’s life as a cannabis farmer:

4. Prohibiting Marijuana Costs Taxpayers $10 Billion Per Year

Over 693,000 individuals are arrested in the US every year for marijuana law violations.

This is far greater than the total number of people arrested for all violent crimes combined, including murder, rape, robbery and aggravated assault.

America has the highest incarceration rate in the world, with one in every 111 adults incarcerated in 2014 in federal, state and local prisons and jails.

That’s 2,224,400 people.

Supporters of marijuana legalization believe laws against its use result in a tremendous waste of criminal justice resources that would be better served in combating serious and violent crime.

NORML wants states to remove all penalties for the private possession and responsible use of marijuana by adults, including cultivation for personal use and casual non-profit transfers of small amounts of it.

Such changes would remove the marijuana smoker entirely from the criminal justice system.

In a June 2005 report by Dr. Jeffrey Miron, visiting professor of economics at Harvard University, replacing marijuana with a system of taxation and regulation similar to that used for alcohol would produce combined savings and tax revenues of between $10 billion and $14 billion every year.

For example, total tax revenues from medical and recreational marijuana in Colorado took in about $7.5 million in August alone of 2014. According to the Colorado Department of Revenue, the state collected almost $70 million in marijuana taxes from July 1, 2014 to June 30, 2015, outstripping alcohol taxes for the same period.

And in September 2014, recreational sales of marijuana exceeded medical sales in Colorado, suggesting that a system of regulation may offer a viable alternative to the black market.

We’ve seen similar results in Washington.

Marijuana sales in Washington exceeded $250 million dollars in 2014/2015, with $62 million collected in tax revenue from legal marijuana sales.

The state’s original forecast was $36 million.

5. Marijuana vs Tobacco: Not All Smoke Is Created Equal

There are many reasons why cigarette smoking is worse for you than marijuana.

Marijuana is not physically addictive like tobacco. This means marijuana smokers generally don’t chain smoke, and so they smoke less.

More importantly, tobacco contains nicotine. Marijuana doesn’t.

New research has shown that it is the nicotine that may cause a lot of the cancer in tobacco smokers and in people who live or work where tobacco is smoked.

This is because it breaks down into a cancer-causing chemical called ‘N Nitrosamine’ when it’s burned and it may do so when it’s inside the body too.

So does smoking marijuana pose similar dangers to your health?

According to a number of recent scientific findings, marijuana smoke and tobacco smoke vary a lot in their health effects.

Marijuana smoke contains multiple cannabinoids, many of which possess anti cancer properties and therefore likely exerts “a protective effect against pro-carcinogens that require activation.”

Renowned cannabis researcher Robert Melamede states that “components of cannabis smoke minimize some carcinogenic pathways whereas tobacco smoke enhances some.”

Research has also so far failed to identify any link between cannabis smoke exposure and elevated risks of developing smoking-related cancers, such as those of the lung and neck.

Preclinical studies show there is no increase in risk for other cancers either, including melanoma, colorectal, lung, prostate, breast and cervical, and this seems to apply even with long-term marijuana smoking.

In fact:

The largest case-controlled study ever to investigate the respiratory effects of marijuana smoking reported that cannabis use was not associated with lung-related cancers, even among those who smoked more than 22,000 joints over their lifetime.

Another study, which tested the lung function of over 5,000 adults aged between 18 and 30, was published in the Journal of the American Medical Association in 2012.

After 20 years of testing, researchers found that regular marijuana smokers (defined as having up to a joint a day for seven years) had no discernible impairment in their lung activity when compared with non-smokers. The study also found that marijuana smokers had a reduced risk of developing head and neck cancers.

And a five year long population-based case-control study found even long-term heavy marijuana smoking was not associated with lung cancer or upper aerodigestive tract cancers.

In fact, researchers were surprised to find that marijuana smokers performed slightly better than smokers and non-smokers alike on the lung performance test.

Why is this?

It’s likely that the act of inhaling marijuana is similar to doing a pulmonary function test, which may give marijuana smokers the upper hand over cigarette smokers.

This study led researchers to suggest that low to moderate use of marijuana is actually less harmful to users’ lungs than exposure to tobacco, even though the two substances contain many of the same components.

6. How Life Insurance Companies View Marijuana Users

Given all of the above, surely it’s no big deal if you partake in the occasional spliff?

You’re not alone if you do.

According to a Gallup poll, pot is America’s number one illegal drug of choice.

So how do life insurance companies really view people who use marijuana either for leisure or for medical reasons?

Despite the growing support and legalization of marijuana, the cultivation, distribution and use of marijuana is still illegal under federal law.

The fact that it is illegal at a federal level is a factor you must consider when choosing a life insurance company, especially one that operates nationally.

Since more US states are supporting and legalizing marijuana, one might think that more life insurance companies would adopt a more relaxed attitude too.

The good news?

Some companies are indeed starting to follow suit.

Prudential is one example of a life insurance company that has adopted a progressive attitude on marijuana use.

Today as of November 2022 Prudential will not rate for any amount of cannabis use with a valid marijuana prescription card.

Back in September 2016, you could use marijuana up to three times per week and still be considered for their top health class rates.

Only three years ago, these top health rates were only offered to those who used marijuana two times per month and applicants had to test negative for THC on their medical exams.

That’s quite a change.

And there’s more good news.

Marijuana use is regulated by HIPAA laws.

Under HIPAA laws, admitting you use marijuana will NOT get you into trouble with the law, even if you live in one of the states where pot is illegal.

There’s nothing to worry about from a legal standpoint in disclosing your use of marijuana on an insurance application, because any medical, health and private information you disclose – including your marijuana use – is private and protected.

It cannot be passed to another entity.

Your personal history of drug use will ONLY be available to the underwriters when determining your rates.

But the question remains: can you still buy life insurance if you use marijuana?

Let’s take a closer look.

According to a survey by Munich American Reassurance Company, occasional marijuana users can avoid paying smoker rates in close to one third of life insurance companies.

Just one in five companies do not yet have an official underwriting policy in place for marijuana users, however, most of them expect to have one soon.

And depending on how often you smoke, your marijuana use might not affect your life insurance rates at all.

How often you use marijuana does count though.

While marijuana is starting to lose its social stigma with some life insurance companies, heavy recreational use can still be counted as smoking, which could cause some applications to be denied.

Does that mean insurance companies aren’t prepared to accept heavier marijuana users that smoke more often? Keep reading to find out.

Life insurance is available for marijuana users with or without a prescription at a Preferred rate class with the right companies. This means that if you’re a recreational marijuana user, you don’t have to hide the fact.

If you have a prescription for medicinal marijuana, you could qualify for lower rates.

Since the job of an underwriter is to view your total health picture, your marijuana use is only part of it.

Having a legal script for medical cannabis is better for your rates than being someone who smokes recreationally just because they feel like it.

This seems fair, right?

You were prescribed marijuana to treat a medical condition, while the other guy just likes to relax and get a little high. That said, an underwriter will still need to know why you received a prescription and what the underlying reasons are for it.

The bottom line?

If your prescription is for a condition that doesn’t normally affect your rates, you’re better off than a casual marijuana smoker. But if it’s for something significant, you’ll be rated based on the normal risks associated with that condition or disease.

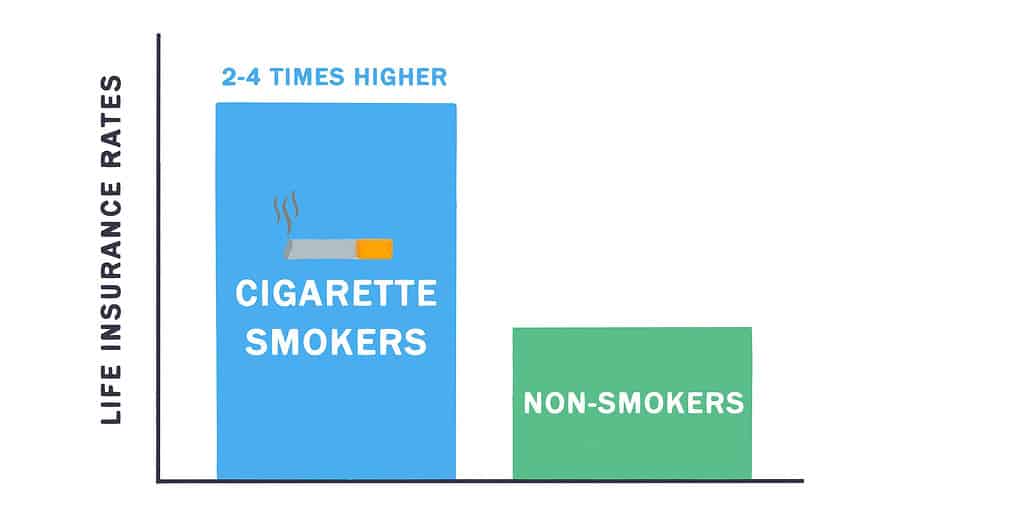

Cigarette smokers pay rates that are two to four times higher rates than those for non-smokers.

So it’s great news that life insurance companies that do have an underwriting policy for marijuana use are no longer grouping marijuana users in the same risk category as cigarette smokers, or worse, declining applications from users altogether.

This means as a marijuana user, you can get approved with a non-smoker’s rate even if you light up occasionally.

Not only are life insurance companies saying marijuana users are less risky than meth users, but that they’re less risky than tobacco smokers too.

Underwriters are now being more flexible with marijuana users, and if you shop around today, you can find a more affordable rate than you could five or ten years ago.

Conversely, about 20% of life insurance companies in America don’t yet have an underwriting policy in place for marijuana users.

That’s why it pays to shop around for marijuana life insurance.

There’s the possibility that some insurers may still view marijuana users as a high risk, along with meth and heroin users, because marijuana is still classified as a dangerous and illegal drug.

Sixteen per cent of Americans have lied about a marijuana habit to get lower life insurance rates, according to a new NerdWallet survey.

The same survey found that lying to a life insurance company about tobacco smoking habits to receive lower rates was deemed as being less acceptable with only 11% saying it was OK.

It’s easy to see why.

A person could save around $1,000 every year on their life insurance if they lie about tobacco smoking, according to NerdWallet’s analysis of average standard rates.

That’s despite the fact that cigarette smokers pose a higher risk to insurers than users of marijuana.

7. Smoking vs Eating Marijuana: Does It Really Matter For Life Insurance Rates?

Another pot conversation that happens is about the potential health risks of consuming marijuana-infused edibles.

From the point of view of life insurance, does it matter if you ingest, inhale, eat, smoke or vape your marijuana?

The short answer is not really.

Maureen Dowd of the New York Times’ was “curled up in a hallucinatory state for the next eight hours” after consuming edible marijuana in the form of a candy bar.

And Forbes says there are reports of ER doctors in Colorado treating more patients for intoxication from pot-infused edibles, not to mention some startling incidents of psychotic behavior and deaths from such products.

Even the Weed Blog advises people to be careful about eating marijuana because you can get way too high if you eat too much.

The ingesting of pot brownies, weed tea and other marijuana edibles has raised concerns about overdosing. This is because they often have higher concentrations of THC, which means the delayed onset of the initial “high” can lead to overconsumption.

So it’s probably no surprise that life insurance companies are not giving any additional leniency if you only eat instead of smoking your marijuana.

However, 49% of underwriters surveyed by Munich American Reassurance Co. said they believe there’s no difference in risk between a marijuana user who smokes the drug and one who ingests it through “edibles.”

Even so, 43% thought that smoking marijuana was riskier than ingesting it, while 8% viewed ingesting it as riskier.

One of the biggest concerns in this regard is how marijuana is absorbed and metabolized and how quickly the high comes on.

Kari Franson, PharmD, PhD, Clinical Pharmacologist and Associate Dean for Professional Education at University of Colorado Skaggs School of Pharmacy says “the major difference is in the absorption of the [edible] product into the blood stream. Once it’s in the blood, it quickly goes to and has an effect on the brain.

With smoking, the peak blood levels happen within 3-10 minutes, and with eating, it’s 1-3 hours. Note that both are about a three-fold difference, but most users are willing to wait 10 minutes, not 3 hours before re-using.”

In other words, the effects of smoked or vaporized marijuana can come on faster and diminish more quickly because the THC travels directly to the brain.

With edible marijuana, it can take anywhere from 30 minutes to two hours before users experience the high. They may thus inadvertently consume an overdose amount while waiting for it to hit.

One thing to note with cannabis-infused edibles is there’s no smoking involved so common sense should suggest precluding insurers from charging smoker rates if people are only ingesting marjuana.

Life insurance guidelines for marijuana users will no doubt continue to evolve, and as the landscape continues to change, life insurers may alter their position on this.

8. The Impacts of Marijuana Use and Life Insurance

Understandably, life insurance companies are still generally conservative when it comes to marijuana use.

Unlike with health insurance, life insurance companies take a more holistic view of an applicant’s lifestyle, from their general health and daily activities to their occupation and the sports and hobbies they engage in.

As we’ve seen already, insurers are adopting more relaxed attitudes about marijuana use, and most are no longer rejecting users outright, despite it still being an illegal drug in some US states.

That said, some life insurance companies still charge pot smokers the same rates as tobacco smokers, while others charge higher rates for pot smokers only if they smoke heavily.

Your use of marijuana will have an impact on your final life insurance rate and depends on several factors, which we will discuss now.

1. How Often You Smoke, Vape or Consume Marijuana

How frequently you smoke, vape or consume marijuana is significant. This is the number one thing underwriters will consider when determining your premiums.

The more liberal insurers will probably categorize you as a non-smoker if you only consume 1 or 2 marijuana joints per month. However, if you apply to the wrong company, you could still be slapped with a smoker’s status.

On the extreme end, there are companies that will flat out deny your application if you smoke eight or more marijuana cigarettes per month.

If you tried it a couple of times 24 years ago in college, it probably won’t matter. But if you’ve been smoking three joints a day for the past ten years, then yes, they will care, and you will pay higher premiums.

2. The Last Time You Used Marijuana

While not nearly as important as frequency, the date of your most recent marijuana use is important for three reasons.

Let’s say you’ve only smoked marijuana twice in your whole life and both times were last week. What does this suggest about the chances of you continuing?

Everyone starts sometime.

The closer your use of marijuana is to your medical exam date, the higher the chance of you testing positive for THC during it.

Let’s just say that a positive test will typically mean higher rates for you.

Plus if you’ve used marijuana recently, it may raise some red flags with the underwriter as to whether you’re telling the truth on your actual frequency or forgetting how often you really do light up.

Like tobacco use, other factors such as your personal and family health history play a critical role in the type of premium you’ll pay.

Your prescription for medicinal marijuana or your recreational habit is only part of the equation in getting you the cheapest rates.

3. Whether You Use Marijuana Recreationally or Medicinally

If you’re a recreational user of marijuana, you’re seen as having no higher risk when compared to someone who uses it for medicinal reasons.

In fact, it could be the opposite.

Health is a major underwriting factor in life insurance, and a marijuana prescription is often an indication of some underlying health concerns.

The underlying medical condition for WHY a person has a prescription for medicinal marijuana will be factored into the underwriting.

This means a person who uses marijuana for medical reasons will be subject to additional scrutiny and underwriting questions.

In other words, insurers want to know what conditions people have that qualifies them for a medical marijuana card.

If you have a prescription for a condition that doesn’t normally affect your rates, you’re better off than the casual marijuana user, but if it’s for something significant, you’ll be rated based on the normal risks associated with that condition or disease.

That doesn’t mean it will affect your final rate, but it’s certainly taken into consideration.

On the other hand, a person who uses marijuana recreationally will likely only be scored on their frequency and date of last use.

9. How To Get Approved For Life Insurance If You Smoke Marijuana

If you’ve been reading this far, there’s a good chance that you are indeed a marijuana user…

…and you’re wondering how you can apply, get approved and get the best rates for life insurance.

If so, you’re probably asking yourself questions such as:

“How much do I need?”

“Will I be tested for marijuana or only nicotine or cocaine?”

“What kind of policy is best?”

“What if I smoke cigarettes too?”

“Which company should I buy from?”

Below are six important tips to help make the process of getting life insurance smoother and to ensure you get the best coverage at the best price.

1. Find a Company That Considers You a Non-Smoker

This is important.

The key is to find a company that will give you non-smoker rates because some life insurance companies treat marijuana smokers as cigarette smokers and will charge tobacco rates accordingly.

This matters because average life insurance rates for smokers are easily three times what they are for non-smokers.

Securing non-smoker rates could cut your premium in half by 50%.

Based on rates for a 20-year, $500,000 policy at ages 35 and 45, women who smoke pay an average of $1,071 more per year for term life insurance than non-smokers, while men pay $1,455 more.

The last thing you want to do is to choose a company that views your marijuana prescription or habit as being high risk, just because they don’t have an underwriting policy in place for marijuana users.

That’s why it’s important to shop around and find a good independent agent who can direct you to companies that are more marijuana-friendly.

Many insurance companies now view smoking marijuana as better than smoking cigarettes so just make sure you apply to the right one.

*Refer to the section below for a list of marijuana-friendly life insurance carriers. Remember, it DOES matter which company you apply to, otherwise your application could get rejected or be lumped in with tobacco smokers.

2. Whatever You Do, Don’t Lie

Let’s say you’re a light marijuana user and you’re able to abstain for a little while so you test as clean on the medical exam.

Do you really have to mention your weed habit on the application?

The answer is YES and here’s why:

- Lying on a life insurance application is fraud.

- There’s a strong chance your application will be rejected if the medical exam reveals the drug in your system and you’ve lied about it.

- You won’t qualify for top rates if your marijuana use is discovered, and in fact, you’ll heighten the insurance company’s suspicion, causing them to dig deeper into other areas of your life and history to see what else might you be hiding.

- Being dishonest in this way and being found out is also grounds for your life insurance policy to be considered void in the event you die.

The health class and corresponding rate you pay for your insurance are based on several factors including your marijuana usage. If you die within two years of the policy date, the insurance company is entitled to investigate before paying the death benefit.

These two years are known as the contestability period.

If evidence turns up that shows you were not truthful on your application, the death benefit to your beneficiaries could be in question.

Your insurer will pull records and if they find any evidence of THC in your history, they have grounds to deny the claim, since you made a material misrepresentation on the application, which would have led them to either deny you coverage or offer it at a different rate.

Do you really want that to happen?

In a best case scenario, they will claim that you should have been approved at a lower health rating (which carries a higher premium). The company will deduct any adjusted premiums before they pay the death benefit.

But in a worse case scenario, they may determine you should have never been approved at all. In this case, the only thing your loved ones will receive is the premiums you paid in but NO lump sum death payout like you had planned to leave them.

But what if marijuana is illegal in your state?

It doesn’t matter. Still don’t lie.

Life insurance companies don’t care whether the state you are living in has enforced marijuana prohibition. They’re more concerned about the medical impact of marijuana.

These days you can get affordable rates as a marijuana user.

If you die during the first two years of your policy and your insurance company investigates, can you stomach the thought of your beneficiaries being denied their money?

3. Disclose Your Usage, How Often You Use and Your Reasons For Using Marijuana

Once you’ve decided to apply for a life insurance policy, you’ll need to go through the application process, which often requires a medical exam, phone interview and underwriting.

The first step is to be upfront and honest with your life insurance agent and to let them know you do use marijuana.

They’re going to check for nicotine products, alcohol, marijuana and other legal and illegal drugs anyway, so you have nothing to lose by being honest.

As noted above, the last thing you want to do is to not disclose your marijuana use and then have it show up on a life insurance medical exam.

If you lie on the application and the insurance company finds out, they may increase your premiums or cancel your policy altogether.

What We, At Simple Life Insure Will Ask You:

At Simple Life Insure, the most frequently asked question we get is:

Do life insurance companies test for drugs?

We believe you deserve to have your life insurance – and the future of you and your family – handled by an independent life insurance broker with your best interest at heart.

We can assure that everything you discuss with us is confidential and we observe all HIPAA laws. Plus, you can choose your own coverage and be positive that your needs will be met.

Here’s what we will ask of you at Simple Life Insure:

- How frequently do you use or consume marijuana products? Do you use marijuana:

- On weekends – no more than twice a week

- Less than three times a week

- Less than four times a week

- More than five times a week

- When was the last time you used cannabis?

- How long have you smoked marijuana for? Since what age?

- Have you ever used other drugs besides marijuana? If so, what/when?

- Have you ever had any legal troubles related to drug use? If so, explain.

- Do you smoke or use tobacco products in addition to pot?

- How do you consume cannabis? Smoke, as edibles, or both?

- What is the reason for your use of marijuana? Purely recreational or to help deal with anxiety, stress, or pain relief?

- Do you have a prescription for medicinal marijuana? If so, what condition is the prescription treating? We then ask the applicant to provide details of symptoms and medical history of this condition.

The next step is to disclose to the agent how often you use marijuana.

This will let you know what rate class you can expect to receive from the various life insurance carriers who underwrite marijuana users.

If you’re a daily user, then make sure that the agent knows that, and if you’re just an occasional user, it’s even more important to give that information.

Next, tell the agent what your reasons are for using marijuana. This is a necessary step as it may get you a lower rate with marijuana-friendly insurance companies.

If you’re using it for pain management or another medicinal purpose, then let them know. If you’re using it for recreational purposes, you’re going to want to tell them that as well.

You’ll also need to describe to the agent how you use marijuana.

For instance, do you smoke it rolled in paper or do you prefer to use a bong or pipe?

You might not use marijuana through inhalation but instead have it in edible and baked goods. Whatever the case, make sure you tell the agent.

4. Send a Cover Letter Explaining Your Marijuana Use With Your Application

This is your opportunity to sell your case to the underwriter, especially when you know you might have issues that will get challenged.

By providing a cover letter with your application that explains why and how often you use marijuana, you give the underwriter a clear and thorough picture from the beginning.

A cover letter like this with a clear intent can help you avoid having your application declined from the outset. An experienced independent broker can draft such a letter for you to increase your odds of a favorable response.

5. Remember That Marijuana Users With a Prescription For Medicinal

Use Might Qualify For the Best Life Insurance Rates

But it depends what condition is being treated, so rates will still depend on health of the applicant.

Medical marijuana can be a double-edged sword.

If a condition isn’t considered serious by the insurer, a person with a marijuana prescription may be treated like a recreational user and get a worse rating.

But if the condition is considered serious – such as AIDS, cancer or severe arthritis – it’s also likely to be uninsurable.

Taking medicinal marijuana for muscle spasms or nerve pain is a lot different than taking it for cancer or multiple sclerosis.

The reason that you have that prescription will drive the underwriting result first and foremost. The use of marijuana itself will be a secondary consideration.

Even if a serious condition is insurable, the cost of the life insurance policy may still be high. Marijuana will not make any difference to that.

6. Remember Too That Recreational Pot Users Don’t Usually

Qualify For The Very Best Non-Smoker Rates

But you can qualify for standard non-smoking rates at some companies.

As we’ve already mentioned, how often you use marijuana matters.

Most insurers will consider you a smoker if you use marijuana more than once a week. If your frequency is less than this, your options to qualify for Preferred rates at select insurance carriers open up.

To wrap this up, you’ll need to answer the following questions to allow an independent broker to help place you with the most suitable marijuana-friendly life insurance company:

- How often do you use marijuana?

- When was the last time you used marijuana?

- What is your method of use, e.g. smoking, ingesting, inhaling, etc.?

- Is your marijuana use for recreational or medicinal purposes?

- If medicinal, what is the nature and severity of the underlying health condition that is being treated?

- Is your marijuana use for recreational or medicinal purposes?

Don’t assume that you can’t apply or get approved for life insurance if you use marijuana. You may qualify for better rates than you expected.

Don’t like needles? Too busy to schedule a medical exam? Smoke cigarettes too? Here’s all the questions you’ve been too afraid to ask

Below are answers to some of our most frequently asked questions about medical exams for insurance.

Can I apply for life insurance without undertaking a medical exam?

You can consider a no medical exam policy but expect to pay more for it.

Because the insurance company doesn’t know much about your health without an exam, they’re taking on a greater risk and the premium for this type of policy will be higher, typically by 10% to 50%.

It’s likely you’ll get a better price if you’re willing to submit to a medical exam, but no exam policies are available if that’s what you prefer to choose.

Do I have to pay for the exam?

No. The life insurance company covers the cost.

Will I have to take another exam if I’m not approved the first time?

If you’re working with an independent broker, your exam can usually be carried over to other insurers.

If you didn’t get approved the first time or received an offer that was too expensive, we’ll shop around to get you a better rate.

If you apply directly with the insurers, you may need to submit to a new exam each time so it pays to go through an independent broker.

How long does the exam take?

Approximately 30 minutes.

Do I have to go into a doctor’s office?

No. A registered nurse will meet you in the comfort of your own home or office.

What will they do at the exam?

The nurse will take a blood sample and urine sample, as well as checking your blood pressure and measuring your height and weight. They’ll also test your cholesterol and glucose levels and they may even do an ECG on your heart.

You could have a mouth-swab, as opposed to a blood test, to check for a range of potential health issues. This is usually non-invasive and painless.

Pro Tip: Find Out How You Can Ace The Medical Exam To Get A Lower Rate.

What is THC?

THC or tetrahydrocannabinol, is the chemical responsible for most of marijuana’s psychological effects. It’s one of many compounds known as cannabinoids that are found inside the resin glands of the marijuana plant.

Interestingly, it’s the female cannabis plant that produces the highest amounts of THC, whereas the male cannabis flower typically doesn’t produce enough to interest most people. In its raw form, THC is found as an acid in the plant.

How long does THC stay in the blood?

While everyone has a theory, there’s no simple answer to this question. THC is fat-soluble, not water-soluble. If THC were water-soluble, all traces would be gone from the body within days.

In fact:

THC can actually increase for days after you’ve stopped using marijuana, according to Paul Armentano, deputy director of the National Organization for the Reform of Marijuana Laws and the NORML Foundation.

Lifestyle factors, including a person’s consumption frequency, are variables that also affect how long marijuana stays in the system.

Armentano cites a study that says THC stays in the body for up to 100 days after it has been consumed, so it could take more than three months before a person has cleared the evidence of marijuana use from his or her system.

Do life insurance companies test for THC?

Yes, since THC is the primary ingredient in marijuana that is responsible for getting you high.

This means your use of weed or marijuana can show up in a blood or urine test.

In most cases, medical exam lab results will show the presence of at least 50 nanoliters of THC metabolites per milliliter of urine. This compares to 15 nanoliters per milliliter for most “official” tests.

What other drugs do life insurance companies test for?

The short answer is they test for everything, including:

- Cocaine

- Nicotine

- Methadone

- Barbiturates

- Amphetamine/Methamphetamine

- Benzodiazepines

- Opiates

- Phencyclidine (PCP).

It is possible to get life insurance even if you’ve struggled with drug and substance abuse in the past.

In the case of addictive drugs, most carriers will require that you remain clean for at least three years with no relapses before they will insure you. This is referred to as a “postponement”. It’s not a denial, but it’s not an approval either. They are basically saying that you should stay clean and check back with them in three years and they’ll take your application then.

The National Institute on Drug Abuse (NIDA) states that relapse rates for addictive drugs are 40%-60% and are even higher when a user has recently quit.

Life insurance companies know these statistics well. It’s their job to know. The more time that has passed since you quit a drug of dependence, the less risk you have of relapse, and therefore the better your chance for approval and lower insurance rates.

I smoke cigarettes AND use marijuana? How will this affect my premiums?

If you do both, you’re most likely looking at receiving smoker rates. It then becomes a question of which carrier is the best for your individual smoking habits.

While both habits will be considered, typically it’s the more frequent of the two that will dictate the underwriting decision.

Anytime you’re dealing with multiple variables that may affect an underwriting decision, there really isn’t a clear-cut answer ahead of time. Again, you’ll need to shop around or work with someone who knows all the carriers and can do the research on your behalf.

I usually ingest marijuana. (In other words, I eat it). Will I still get a smoker rate?

It depends on how often you use marijuana and why.

Most insurance companies are not yet making a distinction between eating it and smoking it, so everything that applies to smoking marijuana will apply to eating it as well.

Many people who ingest marijuana edibles do so because of a prescription. If you are consuming marijuana for medicinal reasons, your medical records will be reviewed and the underlying reason for the prescription will be considered.

If you eat marijuana for recreational reasons then insurers may not request to see your medical records.

In summary, the medical exam is not something to worry about.

It’s designed to be convenient for you, while still obtaining the necessary information for your insurer. It allows carriers to understand your health picture and offer you the correct rate.

10. Marijuana-Friendly Life Insurance Companies

So now you know everything you need about getting life insurance as a marijuana user, where should you apply?

Who will give you the best rates?

Certain marijuana-friendly life insurance companies will offer up to Preferred Plus rates (the best).

Other companies will decline you outright.

You need to apply with the right company from the start or you could be setting yourself up for failure.

The company you apply to makes all the difference in what rate you’ll get and this is what determines your premiums.

The secret to getting the lowest rate is having us place you in a policy with the company that views you in the most favorable light.

We’ve picked the top 16 marijuana-friendly companies that even the heaviest users will want to look at.

Remember, each life insurance company has its own guidelines and underwriting rules, so their views on using marijuana may differ from each other.

All of these companies offer non-smoking rates to marijuana users.

The below table shows the different health classes from best (Preferred Plus) to worst (Table 8). We have included the % increase you can expect to pay at each level.

You can quickly see why it pays to apply with the right company.

| Health Class | Price Increase % |

|---|---|

| Preferred Plus | ------------- |

| Preferred | 20 to 25% |

| Standard Plus | 20 to 35% |

| Standard | 15 to 25% |

| Table 1 | 22 to 27% |

| Table 2 | 22 to 27% |

| Table 3 | 22 to 27% |

| Preferred Tobacco | 5 to 15% |

| Table 4 | 5 to 15% |

| Table 5 | 22 to 27% |

| Table 6 | 22 to 27% |

| Table 7 | 22 to 27% |

| Standard Tobacco | 5 to 10% |

| Table 8 | 5 to 10% |

1. Prudential

Frequency: If you use weed or pot up to three times (3X) per week with a prescription and have a negative lab result, you may get approved at the Prefered Plus non-smoker class.

If you use marijuana between four and six times (4 and 6X) per week, you’re looking at a Table 2 rating, but could still be considered as a non-smoker.

Not acceptable: Anyone using marijuana seven times (7X) or more per week will automatically be declined for life insurance with Prudential.

Testing positive for THC in your lab results won’t affect Prudential’s eventual underwriting decision. However, your application will be turned down if you don’t disclose your marijuana usage on the application and then test positive to it.

Medical exam required: Yes

A.M. Best Financial Rating: A+

Types of policies available:

- Term

- Universal

- Variable Universal

- Whole

2. Lincoln Financial Group

Frequency: You can qualify for non-smoker Preferred Plus rates with Lincoln Financial only if you smoke marijuana once per month (1X).

Those who use marijuana no more than two times per week can get Preferred non-smoker rates.

Standard to substandard non-smoker rates are available to people who use but do not smoke marijuana more than three to six times (3 to 6X) per week.

Not acceptable: Lincoln Financial will deny applications for those who use marijuana recreationally daily.

Medical exam required: Yes

A.M. Best Financial Rating: A+

Types of policies:

- Term

- Universal

- Variable Universal

![]()

3. Columbus Life Insurance Company

Frequency: Standard smoker rates are available from Columbus Life to those whose marijuana use is considered infrequent by the underwriters and who are over the age of 25.

Not acceptable: Testing positive for any level of THC on the medical exam.

Medical exam required: Yes

A.M. Best Financial Rating: A+

Types of policies:

- Term

- Universal

- Indexed Universal

- Variable Universal

![]()

4. Fidelity Life

Frequency: Fidelity Life may offer Standard smoker rates to people who have used marijuana in the past twelve months.

Not acceptable: Received any treatment for drug abuse in past 10 years.

Medical exam required: Exam and no-exam options are available

A.M. Best Financial Rating: A-

Types of policies:

- Term

- Whole

- Hybrid

5. Genworth Financial

5. Genworth Financial

Frequency: Those who use marijuana eight times (8X) per month or less can get Standard smoker rates from Genworth. Anyone using it more than eight times (8X) per month will be considered the same as a Substandard smoker.

Not acceptable: Prescription use is not recognized or considered any different.

Medical exam required: Yes

A.M. Best Financial Rating: B++

Types of policies:

- Term

- Universal

- Whole

- Index Universal

6. ING (Voya) Life Insurance

Frequency: Even with daily marijuana use, you can be approved at Preferred smoker rates, although a number of other factors will also determine your eventual premium. Marijuana use less than two times (2X) per month will be classed as a Standard non-smoker.

Medical exam required: Yes

A.M. Best Financial Rating: A

Types of policies:

- Term

- Universal

- Whole

- Index Universal

- Variable Universal

7. Minnesota Life

7. Minnesota Life

Frequency: Using marijuana less than once a month or twelve times (12X) per year and your test for THC is negative, you can qualify for Minnesota Life’s Preferred non-smoker rate.

Not acceptable: A positive test for THC on medical exam disqualifies the applicant for non-smoker rates of any kind.

Medical exam required: Exam and no-exam options available

A.M. Best Financial Rating: A+

Types of policies:

- Term

- Universal

- Index Universal

- Variable Universal

- Whole

8. North American Company

Frequency: Applicants who smoke marijuana up to eight times (8X) per month can be approved at Standard smoker raters. Use up to sixteen times (16X) per month can be considered but only at Substandard rate classes.

North American may still offer you life insurance if your usage is as high as sixteen times per month, but it will cost you, and you should expect Substandard table rates.

Not acceptable: Marijuana use greater than sixteen times (16X) per month.

Medical exam required: Exam and no-exam policies offered

A.M. Best Financial Rating: A+

Types of policies:

- Term

- Universal

- Indexed Universal

9. Protective

Frequency: Recreational users of any marijuana frequency will receive Standard non-smoker rates with a negative lab test for THC. Prescription users may be approved at Standard non-smoker rates, depending on their underlying medical condition.

Not acceptable: Postive THC test for recreational users.

Medical exam required: Yes

A.M. Best Financial Rating: A+

Types of policies:

- Term

- Universal

- Variable Universal

- Survivorship Universal

![]()

10. TransAmerica Life Insurance Company

Frequency: Transamerica offers Standard smoker rates to recreational users. Even frequent usage can be approved at Standard smoker rates. Non-smoker rates may be available for some medicinal prescription users depending on the medical condition in question, the frequency of marijuana use and the method of consumption.

However, you could be stuck with smokers rate or lose out on coverage altogether if you use marijuana more than nine times per month.

Not acceptable: Recreational use if you are seeking non-smoker rates.

Medical exam required: Offering no-exam and exam policies

A.M. Best Financial Rating: A+

Types of policies:

- Term

- Universal

- Variable Universal

- Whole

11. SBLI

Frequency: It is possible to get Preferred non-smoker rates as a marijuana user if you use it up to three times (3X) per year. Any more than that, and you’re looking at Standard smoker rates. Depending on the condition for which marijuana is prescribed, medical users will be rated at Table 4 or lower.

Not acceptable: Regular use (recreational or prescription) for non-smoker rates.

Medical exam required: No-exam and exam options available

A.M. Best Financial Rating: A+

Types of policies:

- Term

- Whole

12. Accordia Life

Frequency: Eligibility for insurance with Accordia Life varies according to your age. Those ages 26-30 who use marijuana no more than once a week can qualify for Preferred Plus, which is Accordia’s top rate. Usage of up to three times (3X) per week for this age group will result in a Standard non-smoker rate, while anything higher will be declined.

People older than thirty whose use of marijuana is no more than three times (3X) per week can obtain a Preferred non-smoker rate class, and even daily pot smoking can qualify you for the Standard non-smoker health class.

Not acceptable: Any usage for applicants under the age of 25.

Medical exam required: Yes

A.M. Best Financial Rating: A-

Types of policies:

- Term

- Universal

- Indexed Universal

![]()

13. MetLife

You can get top life insurance rates if you smoke no more than once per week.

Preferred Plus non-smoker rates from Met Life are available to those who use marijuana no more than four times per month. Use at four times per week can qualify you for Standard non-smoker rates and sometimes even higher, depending on an overall case picture.

Frequency: Up to one time (1X) per week may still qualify for top rate class, Preferred Plus non-smoker. Four times (4X) per week can qualify you for Standard non-smoker rates.

Not acceptable: Heavy usage. Daily is a likely decline.

Medical exam required: No-exam and exam options available.

A.M. Best Financial Rating: A+

Types of policies:

- Term

- Universal

- Variable Universal

- Whole

14. AIG

Frequency: If you use marijuana just two times (2X) a year or less, you can qualify for AIG’s top Preferred Plus non-smoker rates, and Standard non-smoker rates are available to those who smoke marijuana no more than twice (2X) per month. Any usage above this means you’re considered a smoker. As such, you may be subject to a table rating.

Not acceptable: More than 2X per month for non-smoker rates.

Medical exam required: A medical exam is required

A.M. Best Financial Rating: A-

Types of policies:

- Term

- Universal

- Indexed Universal

15. Banner Life

Frequency: Occasional users of marijuana can qualify for Banner Life’s Standard smoker rates, although this carrier is somewhat subjective in their definition of “occasional”. They review this on a case by case basis.

Not acceptable: Daily pot users will be considered for Substandard Table B Smoker rate (which is expensive)

Medical exam required: Both exam and no-exam options are available

A.M. Best Financial Rating: A+

Types of policies:

- Term

- Universal

16. Mutual of Omaha

Frequency: You can qualify for Standard non-smoker life insurance rates at Mutual of Omaha if you use marijuana no more than once per (1X) week and your lab tests are consistent with this level of usage.

Prescription users will be substandard Table 3 or lower, dependent on underlying medical issue.

Not acceptable: Regular (daily use) is a decline.

Medical exam required: Both no-exam and medical exam options available

A.M. Best Financial Rating: A+

Types of policies:

- Term

- Universal

- Whole

As we’ve seen, the attitudes of life insurance companies to marijuana use has certainly progressed over the past decade, which is a testament to how far the marijuana legalization movement has grown beyond its hippie roots.

As we’ve seen, the attitudes of life insurance companies to marijuana use has certainly progressed over the past decade, which is a testament to how far the marijuana legalization movement has grown beyond its hippie roots.

Even so, if you use marijuana more than four times per week, you’ll almost certainly be looking at tobacco smoker rates from most insurers, with the exception of a few select companies.

In this situation, the best approach is to not focus so much on the pot.

Your cheapest rate will come from the company who looks most favorably on everything in your history, NOT just your use of marijuana.

Obtaining Life Insurance Can Be Difficult If You Choose To Go It Alone

Now, it’s important to me that you don’t just skim this guide and then pop on over to Facebook.

I want you to actually use the information here to get the best value for your buck.

We’re one of the rare independent brokers that only sells life insurance.

With access to all the top rated life insurance companies, we can help secure you the best coverage for you and your family at the best rates you can afford.

We know this market inside out, so if you’re a marijuana user looking to buy life insurance, don’t go it alone against the big insurance companies.