Life Insurance with High Cholesterol: How to Pay Low Rates

Fact: Cholesterol levels are the #1 reason for life insurance denials and approvals coming back at much higher rates than expected.

Fact: Cholesterol levels are the #1 reason for life insurance denials and approvals coming back at much higher rates than expected.

Some people are aware of their cholesterol levels, and others are unpleasantly surprised at the results of the medical exam.

Each insurance company has different guidelines and rules for how they view high cholesterol (also known as hyperlipidemia).

Great news! This article will tell you everything you need to know in order to pay the lowest rates when shopping for life insurance if you have high cholesterol.

The following questions will be answered:

- How do life insurance providers view high cholesterol?

- What questions will be asked about my cholesterol levels?

- What health rate class will I be in?

- How much does life insurance with high cholesterol cost?

- Best insurance companies for high cholesterol

You are not alone. 73.5 million adults in the United states have high or “bad” cholesterol. Fewer than 1 in 3 of these people have their cholesterol levels under control. You are also not alone in the life insurance maze.

In a hurry? We can help you apply at the right insurance company based on your specific needs and situation. This will not be the same company for everyone. We have experience finding the lowest premiums for our clients with high cholesterol levels. We WILL do the same for you. No pressure or cost to use our expertise.

How Do Life Insurance Providers View High Cholesterol?

The job of a life insurance underwriter is to judge risk.

Cholesterol levels are an important health benchmark used by insurance companies in determining health and rates. High cholesterol has been proven to lead to more serious health issues such as:

- Stroke

- Heart attacks

- Coronary artery diseases such as arteriosclerosis

If you have any of the below conditions or situations, expect insurers to be more cautious regarding your cholesterol levels. These risk factors are often associated with high cholesterol and influence your levels for the worse.

On the bright side, some of these same factors are things you can focus on to improve your chances of paying lower rates.

- Being overweight – can increase triglycerides and decrease HDL

- Diet high in saturated and trans fats

- Smoking – can lower HDL cholesterol

- Lack of exercise or physical activity – lowers HDL

- High blood pressure – can damage arteries and increase the buildup of plaque

- Medications – Some medications can raise triglycerides and lower HDL levels. Medicines such as beta-blockers, estrogen, corticosteroids, and thiazide diuretics.

- Certain diseases – Hypothyroidism, chronic kidney disease, and some types of liver disease. The presence of these can raise the risk of high cholesterol.

- Diabetes – may increase LDL and lower HDL cholesterol

Optimal Cholesterol Levels

Cholesterol and triglycerides are fatty substances found in the bloodstream. When the level of lipids is high, this is known as hyperlipidemia. Hyperlipidemia can lead to a build-up of the lining of the blood vessels. Ultimately, this prevents oxygen from reaching the heart. As you can imagine, this is a serious concern when applying for life insurance.

To determine risk, the following levels will be measured in your blood:

- Total cholesterol

- LDL

- HDL

- Total Cholesterol to HDL ratio

- Triglycerides

Optimal levels that will NOT have an effect on your life insurance premiums are:

| Total Cholesterol | Less than 200 mg/dl |

| LDL | Less than 100 mg/dl |

| HDL | Over 40 |

| Total Cholesterol to HDL ratio | Less than 3.5 |

| Triglycerides | Less than 150 mg/dl |

Good news: If you had high cholesterol levels in the past that are now under control, you don’t need to worry. The insurance company will review your history. As long as the cholesterol levels are not related to another medical condition, you won’t be penalized. Expect the effect on your rates to be very minimal (if any).

Good news: If you had high cholesterol levels in the past that are now under control, you don’t need to worry. The insurance company will review your history. As long as the cholesterol levels are not related to another medical condition, you won’t be penalized. Expect the effect on your rates to be very minimal (if any).

What Questions Will Be Asked About My Cholesterol Levels?

Keep in mind: While very important, cholesterol levels are only 1 of many factors insurance companies look at when making a decision. Your insurance application will ask about your overall health picture and history.

Specific to your cholesterol levels, expect to be asked the following:

- Date of the first diagnosis with high cholesterol

- What are you doing to control it?

- Medications taken for cholesterol

- Family history of heart disease, coronary artery disease, or stroke?

- Any higher than normal blood pressure readings or hypertension diagnosis?

- Most recent results: total cholesterol, LDL/HDL, triglycerides, total to HDL ratio

- Any tobacco use?

A qualified life insurance professional will brief you on all these questions ahead of time so you are prepared. The more they know about your cholesterol levels (and everything else) the more prepared they will be to shop you to the right companies to secure the lowest rates.

Always be completely upfront with your independent broker. They work only for you and NOT the insurance companies.

What Health Rate Class Will I Be In?

2 most important things to know:

#1 – Each company has different guidelines and levels that they look at. This is “negotiable” if you know how to work with the underwriters.

For example: Insurance company ABC may generally not allow LDL levels to be above 125 mg/dl to qualify for Preferred rates. However, if an individual has an exceptionally high level of “good” cholesterol (HDL), they may allow more flexibility. All companies differ.

#2 – The most important level will always be your total cholesterol to HDL ratio.

Assuming no other health issues, our experience has shown the following general guidelines for expected health classes…

Note: The below ratings assume no cigarette or tobacco use of any kind. If you do smoke, please refer to our guide on tobacco use and life insurance. We highly suggest having a chat with us to determine the best options. Multiple variables are trickier and must be approached cautiously to secure approvals.

| Health Class Rating | Cholesterol Ratio | Total Cholesterol |

|---|---|---|

| Preferred Plus | Below 5.0 | Below 250 mg/dl |

| Preferred | 5.1 to 6.4 | Below 300 mg/dl |

| Standard Plus | 6.5 to 7.4 | Below 300 mg/dl |

| Standard | 7.5 to 8.0 | Below 300 mg/dl |

| Table 2 | 8.0 + | 300 + mg/dl |

| Table 5 | 9.5 + | 300 + mg/dl |

How Much Does Life Insurance with High Cholesterol Cost?

Based on the health classes we’ve mentioned already, below are some sample rates…

Sample rates for a 32-year-old male nonsmoker on a 20-year term

| Health Class | $250,000 | $500,000 | $750,000 |

|---|---|---|---|

| Preferred Plus | $13.91 per month | $21.20 per month | $29.54 per month |

| Preferred | $17.19 per month | $28.35 per month | $39.27 per month |

| Standard Plus | $20.56 per month | $35.00 per month | $49.87 per month |

| Standard | $24.19 per month | $42.28 per month | $49.87 per month |

| Table 2 | $28.22 per month | $49.87 per month | $72.18 per month |

| Table 5 | $39.70 per month | $72.18 per month | $105.65 per month |

Sample rates for a 40-year-old female nonsmoker on a 20-year term

| Health Class | $250,000 | $500,000 | $750,000 |

|---|---|---|---|

| Preferred Plus | $15.68 per month | $25.64 per month | $38.06 per month |

| Preferred | $19.43 per month | $33.64 per month | $47.84 per month |

| Standard Plus | $25.29 per month | $44.54 per month | $63.27 per month |

| Standard | $29.88 per month | $52.98 per month | $76.84 per month |

| Table 2 | $34.73 per month | $63.27 per month | $92.14 per month |

| Table 5 | $49.33 per month | $92.14 per month | $135.45 per month |

Table ratings are a group of 8-10 sub-standard classifications used by the life insurance companies. If your health lands you in this area, you WILL pay more.

Table ratings are a group of 8-10 sub-standard classifications used by the life insurance companies. If your health lands you in this area, you WILL pay more.

However, just the difference of 2 levels will mean a price saving of 50% on top of the Standard rates. It pays to apply to the company that is best for your situation.

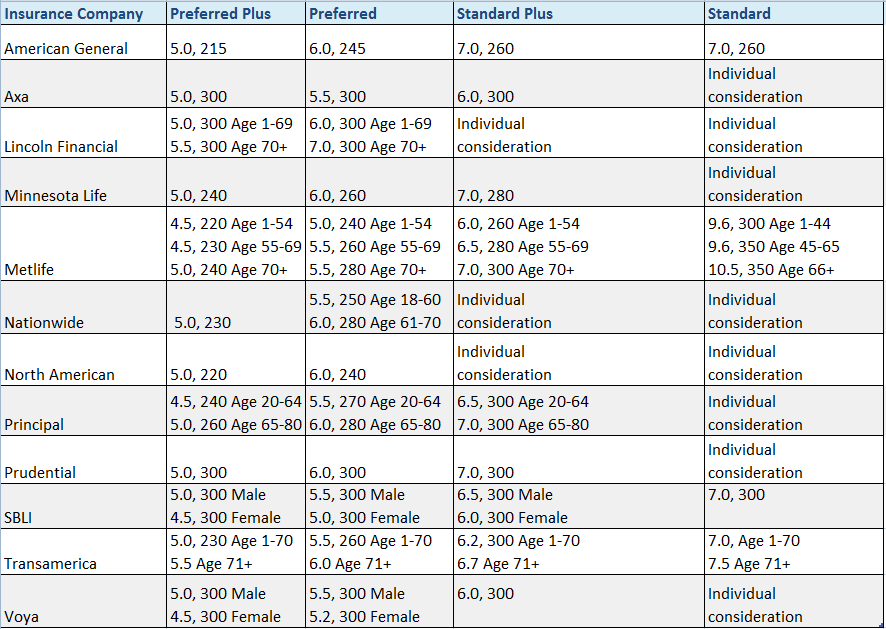

Best Insurance Companies for High Cholesterol

If you have high cholesterol and would like to pay the lowest rates, you MUST apply at the right company.

We have discussed the general life insurance industry guidelines for cholesterol levels as they relate to health classes. These health classes dictate the rates you will pay.

Each company will have their own specific underwriting guidelines as it relates to life insurance approvals and high cholesterol. The below chart shows the carriers we have found to be the most favorable for getting approved at lower rates despite higher than normal levels.

We have also written an article that is specific to Prudential.

A few things to note about this chart:

- The numbers reflect the maximum cholesterol to HDL ratios and total cholesterol allowed to be considered for each health class. Total cholesterol is more flexible and will vary with some carriers based on how low the ratio is. The lower the ratio, the higher the total cholesterol that will be accepted.

- Some insurance providers allow higher levels for older ages or male vs female. These are noted where applicable.

- All the carriers listed below DO allow cholesterol medication to still qualify for the top rate class. (others not on this chart, do not)

- Other health concerns besides the high cholesterol will need to be considered separately and may affect your health class.

- They are not ranked in order (alphabetical)

Worth repeating…the above are guidelines HOWEVER, it is possible to negotiate with some underwriters and “trade” a lower ratio for a credit against higher total cholesterol.

Just because you fall right outside a specific number or range doesn’t mean you are locked in. This is where an experienced independent broker can fight for you with their knowledge of the industry. Your piggy bank $$ will thank you!

Get Coverage Despite High Cholesterol Levels

If you are serious about finding affordable life insurance with high cholesterol, we can help.

There is NO reason to go it alone vs the big insurance companies.

The secret to finding the best coverage is:

- Knowing all the insurance carriers underwriting guidelines, inside and out.

- Working directly with the underwriters.

We know EXACTLY how to do this. We can help if you are ready. There is NO cost to use our service and life insurance is all we do, every day, all day long.

We welcome the opportunity to have a no-pressure chat about your options.

I hope your day is going well.