How to Buy Life Insurance When You Have Cushing’s Syndrome

Wondering how to buy life insurance when you have Cushing’s syndrome?

You’re at the right place.

Here we clarify how to apply to get the best coverage for the lowest rates.

Cushing’s syndrome may be rare, but it’s usually not fatal. However, it can cause serious health problems. To get the coverage you need at the most affordable rates, it’s important to apply to the right company for your situation.

How do you know where to apply?

All companies will require detailed information about past and current medical problems. When you have Cushing’s syndrome, you can be sure that your application will be carefully scrutinized before you’re quoted a rate or issued a policy.

Although this may sound worrisome, applying to companies who view Cushing’s more favorably than others will help you get the best policy. We’ve helped many clients with Cushing’s buy life insurance. We know how each company views the condition and where to apply but first, we have to determine your health status.

Below we explain why insurers will examine your application so carefully.

How Life Insurance Underwriters View Cushing’s Syndrome

Cushing’s syndrome is a chronic yet treatable health condition, with about 200,000 cases per year. It occurs when the steroid hormone cortisol is too high for a long time.

If it’s treatable, why is it so hard to buy life insurance?

It depends on what the cause of the syndrome is, your current health condition, and your risk of medical complications.

Cushing’s syndrome is most commonly attributed to the use of steroid medications, but also happens when adrenal glands make too much cortisol, as well as other causes:

Exogenous Cause:

- Use of glucocorticoids, which are used in allergy, asthma, and skin medications

Endogenous Causes:

- Pituitary tumor

- Adrenal tumor

- Body makes too much cortisol

- Cancer

When Cushing’s syndrome is due to a pituitary or adrenal tumor, it’s called Cushing’s disease.

Underwriters review applications to determine how great the risk of insuring you will be. For example, if glucocorticoids caused your Cushing’s syndrome, the application will be looked at much differently than if it was caused by cancer.

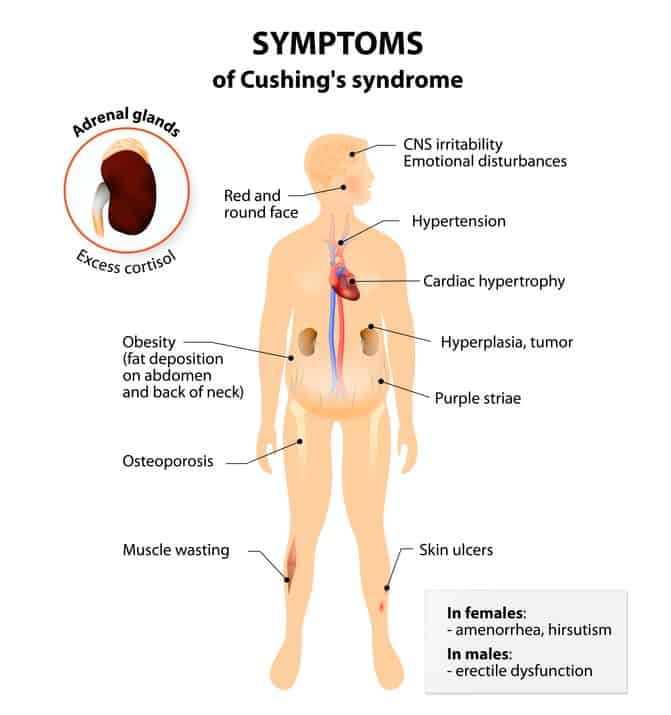

Cushing’s Symptoms – What Life Insurance Companies Want to Know

When you apply, you’ll be required to disclose your health history. It’s important to be thorough, so no information is omitted. If significant information is left out, underwriters will question why and that may complicate the application process or lead to a denial.

Here are some common Cushing’s symptoms they look for:

- High blood pressure

- Diabetes

- Weak bones

- Weight gain

- Infections

- Menstrual irregularity

- Leg and feet swelling

- Memory and concentration problems

- Insomnia

- Fatigue

- Round or moon face

- Red complexion

- Thin skin

- Hair loss

- Bruising

- Depression

- Sweating

- Abnormal fat pad between the shoulders

This is not an exhaustive list of all symptoms, and not everyone suffers from them all. Just know you’ll need to be prepared to answer a lot of questions about your medical condition.

Health Information You’ll Need for the Application

When you apply, you’ll be required to answer health questions, such as:

- Date of diagnosis

- Name of your treating physician/s

- What your current symptoms are

- What medications you’re taking

- What tests you’ve had (lab, ultrasound, MRI, CT scan, etc)

- The cause of your condition

- If you’ve ever had surgery

- If you’ve ever been hospitalized

- What complications you’ve had

- Height and weight

- If you smoke or drink alcohol

- All other medical conditions

This is your opportunity to explain how controlled your syndrome is. Life insurance companies want to be sure you are managing your health, what your overall health condition is like, and if you’re currently under a doctor’s care.

How to Get the Best Life Insurance Rates when you have Cushing’s Syndrome

The bottom line is that no matter how well controlled your Cushing’s syndrome is, knowing how different life insurance companies view this condition is crucial to your being offered a policy at the best rates possible.

Your past and current health status will determine which health class you’ll be assigned to. The health class assigned determines how much you’ll pay for insurance.

For example, if you’re Cushing’s syndrome is not controlled and is causing high blood pressure and weight gain, you won’t qualify for the preferred rate class.

However, if your overall health is good and years ago, surgery treated your Cushing’s syndrome, you’ll be placed in a better rate class than a person with diabetes.

The following is a list of each rate class and what you can typically expect to qualify for.

The best or preferred rates: Not possible

Preferred: Usually not possible

Standard: May be possible after corrective surgery

Table Rating (Substandard): Ratings depend on applicants overall health status

Choosing the Right Company is How to Get Affordable Coverage

All life insurance companies view health conditions differently.

If you’ve been previously denied, it’s still possible to buy life insurance at affordable rates. Knowing where to apply is the most important tactic to prevent denials and sky-high premiums.

We specialize in helping people find the best company their individual needs. We’d love to help you too. There is no charge for our service. To get started or ask a question, please feel free to contact us today by filling out a quote form to get started.