Life Insurance Approval with Hypoglycemia

Most people are familiar with diabetes, which is high blood sugar levels.

Not nearly as many know much about hypoglycemia, which is low blood sugar levels.

But millions of people actually have the condition. You can usually be approved for life insurance with hypoglycemia, but the severity of the condition will determine how much you’ll pay for the policy.

What is Hypoglycemia?

Hypoglycemia is low blood sugar. It’s the opposite of diabetes, which is excessive blood sugar, though it is commonly associated with diabetes. Low blood sugar occurs when your body doesn’t have enough sugar to use as fuel.

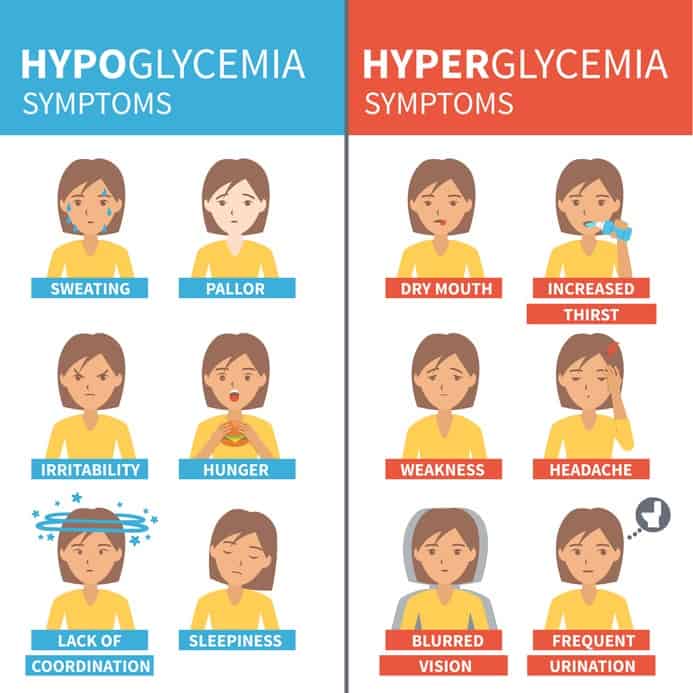

Symptoms of hypoglycemia include:

- Confusion

- Dizziness

- Feeling shaky

- Hunger

- Headaches

- Irritability

- Pounding heart and racing pulse

- Pale skin

- Sweating

- Trembling

- Weakness

- Anxiety

More pronounced symptoms can include poor coordination and concentration, numbness in the mouth and tongue, passing out, nightmares, and at the extreme, coma.

What Causes Hypoglycemia?

Hypoglycemia can be caused by dietary issues, exercise, and certain types of medications, usually, those linked to the treatment of diabetes. The condition can sometimes be controlled by changing those medications.

In some cases, hypoglycemia is caused by insulin treatments.

Apart from diabetes medications, you can also develop hypoglycemia from drinking alcohol, taking aspirin, or combining warfarin with diabetes medications.

Diet can also be a cause. It can develop if you take too much insulin for the amount of carbohydrates you eat and drink. This could include meals that have a lot of simple sugars. It can also be caused by missing a snack, or if you eat less than a full meal, or if you eat later than usual. It can also happen if you drink alcohol without eating any food.

Treatment involves eating less sugary food and eating more frequent but smaller meals throughout the day. If you are on insulin, the doctor can also adjust the dosage to minimize the likelihood of hypoglycemia.

Blood sugar levels can be increased quickly by eating three or four glucose tablets or consuming a tube of glucose gel. It can also be accomplished with several pieces of hard candy, fruit juice, skim milk, a sweetened soft drink, or a tablespoon of honey.

How Life Insurance Companies Underwrite Applicants with Hypoglycemia

With extreme episodes of hypoglycemia, you could experience fainting. That would be dangerous were it to happen while you’re driving. The symptoms can be exacerbated by consumption of alcohol. Insurance companies have to take these situations into consideration in evaluating your policy.

In most cases, you will be able to qualify for life insurance with hypoglycemia.

As is the case in virtually every other health condition, hypoglycemia varies in severity from one person to another. It’s actually a common health problem, affecting millions of people. In many people, the symptoms are very mild, while others can experience debilitating attacks (seizures and fainting episodes).

The biggest concern for insurance companies is the likelihood that hypoglycemia is a direct result of diabetes. It may be that your policy application is declined or charged a higher premium because of diabetes, and not because of hypoglycemia.

The insurance underwriter will be concerned with the following issues:

- When you were first diagnosed with the condition

- How severe the condition is (or how low your blood sugar levels go)

- What are the symptoms?

- Treatments and therapies being pursued

- The prognosis of the condition

The underwriter will also look closely at your weight/height ratio (BMI), your activity level, and whether or not you are a smoker. You will naturally be asked to submit to a medical exam.

If you are unable to qualify for a medically underwritten life insurance policy, you can consider a no medical exam or a guaranteed issue policy. Either will be more expensive than a medically underwritten policy on a per thousand basis. But it may be the difference between getting a policy, and having no coverage at all.

Getting Life Insurance with Hypoglycemia

For the purposes of getting life insurance – and of course, for your own health – it’s vitally important that you’re being proactive in treating hypoglycemia. In all but the most extreme cases, hypoglycemia is managed by lifestyle changes, and by patient response to an oncoming episode.

If you have the condition, you should be seeing your doctor on a regular basis. You should also be taking any medications for the condition, or for related health issues that may be contributing to it.

But most of the treatment is behavioral and relates primarily to diet.

That should include eating lighter but more frequent meals. They should be spaced no more than four or five hours apart. You should never go more than a few hours without eating. The basic idea is to maintain balanced blood sugar level. This is also done by eating the right foods, including plenty of proteins, and sugars only when necessary.

You should also have a ready supply of emergency glucose sources for when your blood sugar level drops. These can include glucose tablets, tube glucose gel, fr hard candy. They should be available anytime you sense they’re needed. It’s important to know your body’s reaction, and to stay ahead of low blood sugar levels wherever possible.

Naturally, you’ll also want to be sure that your overall health is good. That means maintaining proper body weight, getting regular exercise, and avoiding habits like smoking and excess alcohol consumption.

An Independent Life Insurance Broker is Your Best Option for Hypoglycemia

Hypoglycemia is almost a gray area in the life insurance industry.

Some companies attach high significance to it, and will either charge very high premiums, or decline your application outright. Others see it as a manageable condition, and will be highly likely to approve the application, and often at a very reasonable rate.

The dilemma for consumers is knowing the insurance companies that take the most favorable view. As insurance brokers, who work with dozens of different life insurance companies, we know the companies that have the most favorable view of hypoglycemia (today, because it changes) and many other health-related conditions.

That will make all the difference.

Finding the right life insurance policy for consumers is what we do. Put our experience to work for you, and let us find the best policy at the lowest price possible. Give us a call, or complete the quote request form to the left of this article.