Best No-Exam Life Insurance Companies of 2026

I created this in-depth no medical exam life insurance guide because I know how confusing it is to compare term life insurance plans.

Things change fast, and information can quickly become outdated. I’ll continue to update this guide so you always have the most current and accurate information available – so that you can make informed decisions in protecting your loved ones.

No Exam Carrier Comparison Chart

| Company Name | How much does it cost? | How quick is the approval process? | How much coverage is available without an exam? | How financially strong is this company? (A.M. Best Rating) | Will they need to review my medical records? |

|---|---|---|---|---|---|

|

|

$$ | 3 days up to 3 weeks if medical records required. | $50,000-$400,000 | A | Sometimes. At discretion of underwriter. |

|

|

$ | 48 hours up to 30 days if medical records required. | $50,000-$250,000 | A | Sometimes. At discretion of underwriter. |

|

|

$$$$ | 1 week up to 30 days if medical records required. | $50,000-$350,000 | A- | Sometimes. At discretion of underwriter. |

|

|

$$$ | Within 24 hours | $25,000-$250,000 | A- | No. Never. |

|

|

$$ | 15 minutes | $50,000-$400,000 | A | No. Never. |

|

|

$$$ | 1-3 weeks | $25,000-$400,000 | A+ | Sometimes. At discretion of underwriter. |

|

|

$$ | Same day up to 3 weeks if medical records required. | $50,000-$500,000 | B | Depends on policy choosen. |

|

|

$ | 48 hours up to 4 weeks if medical records required. | $50,000-$1,000,000 | A+ | Sometimes. At discretion of underwriter. |

|

|

$$ | a few minutes | $50,000-$1,000,000 | A | No. Never. |

|

|

$ | 1 day up to 30 days if medical records required. | $100,000-$500,000 | A+ | Sometimes. At discretion of underwriter. |

|

|

$$ | 7 days up to 30 days if medical records required. | $25,000-$249,999 | A+ | Sometimes. At discretion of underwriter. |

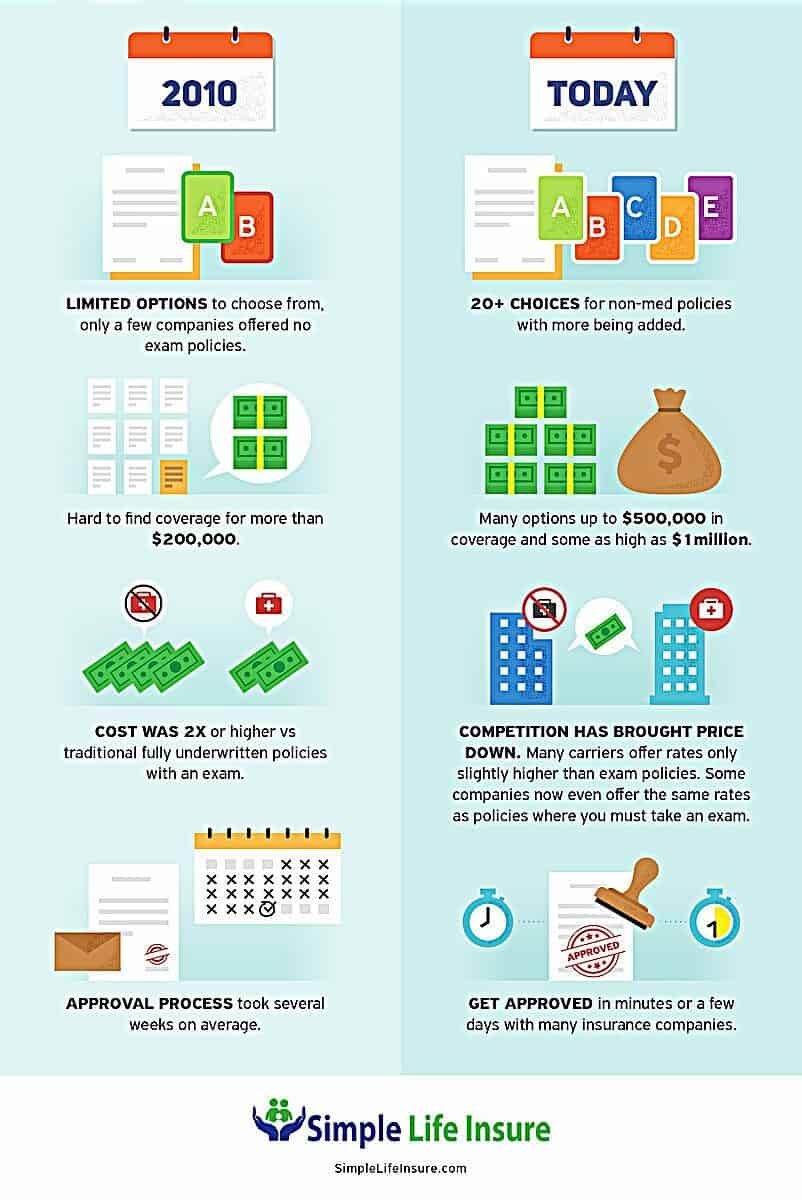

What Does "No Medical Exam" Really Mean?

No medical exam insurance is a policy that does not require a medical exam. There is still underwriting, so it doesn't mean you can hide bad health.

The policy is best suited for shoppers who are in excellent health and in their 50s or younger. However, it doesn't mean insurance companies will turn you away if you don't fall under these criteria. On the contrary, your insurance provider may ask you to answer a health questionnaire, and in some cases, you still skip the medical exam.

Most of the process is done electronically, checking several different database records. This means the decisions are much quicker, and nobody comes to your house with a needle to draw blood.

Many companies are now offering up to $500,000 coverage for no medical policies. If you need more than that, you can combine multiple policies, which is totally fine, and we see it all the time.

Compare quotes right here from 20+ different non-med insurance providers.

How Much Does Term Life Insurance Cost When Skipping the Exam?

Probably not as much as you think.

You no longer have to pay a ton for the privilege of bypassing the medical exam. These days, good life insurance coverage from reputable companies can be found pretty cheap.

In fact:

Some companies now offer the same rates as their fully underwritten products.

We did a pretty extensive study comparing thousands of rates to find how much more consumers pay for life insurance without the annoying exam.

We found that for some, it's the same, not a penny more. On average, it was 10-15% more expensive.

Best No-Exam Life Insurance Companies for 2026

Foresters - Your Term

Advantages:

Disadvantages:

In 2017, Foresters really stepped up their game in the non-med space and is currently one of our most popular choices for life insurance without an exam. Rated "A" (excellent) by A.M. Best means there are no concerns this company will be around to pay out claims.

One great thing is the underwriting process. It's fast, all digital, and they don't need to review your doctor's records. Decisions come back within 15 minutes.

Foresters includes living benefits for critical illnesses and still manages to be one of the cheaper term life products that don't require a physical.

The underwriting department is rather forgiving for several medical conditions, allowing approvals for which other carriers would deny or charge more.

The only drawback we can think of is the lack of Preferred health classes for the non-med "Your Term" product. If you are in excellent health, you may find cheaper premiums at another company.

Foresters also has a final expense product that is used to cover burial and other funeral expenses – this is whole life insurance.

For more info, read our breakdown of Foresters No Exam Term Life Insurance.

Sample No Medical Exam Term Rates - Foresters

40-year-old male at Standard health class - pricing per month

| Coverage Amount | 20 year | 25 Year | 30 year |

|---|---|---|---|

| $50,000 | $17.94 | $22.49 | $26.34 |

| $100,000 | $29.75 | $38.85 | $46.55 |

| $250,000 | $65.19 | $87.94 | $107.19 |

35-year-old female at Standard health class - pricing per month

| Coverage Amount | 20 year | 25 Year | 30 year |

|---|---|---|---|

| $50,000 | $12.91 | $15.09 | $16.97 |

| $100,000 | $19.69 | $24.06 | $27.83 |

| $250,000 | $40.03 | $50.97 | $60.37 |

Penn Mutual

Advantages:

Disadvantages:

If you’re over 50 and looking for no-medical insurance with generous coverage - consider Penn Mutual. The company’s coverage limit is quite high compared to its competitors and reaches up to $7.5 million. And this policy does not demand a medical exam. Note that people up to 65 years old can only qualify.

Penn Mutual policies seem very advantageous, but its website could be equipped with useful tools like generating an instant quote based on your preferences and data. This feature is common among other insurance companies. In the case of Penn Mutual, it’s better to rely on the phone call to your agent to ask for all the current information.

Principal Life Insurance

Advantages:

Disadvantages:

Principal offers a unique twist on the no-exam marketplace. This is their regular term life insurance product, but a portion of applicants will be considered for the accelerated underwriting program. This does require excellent health and is only for Preferred levels.

If you are fit for the program, you are approved electronically within 2 days and don't pay any extra. The rates are literally the same as someone who went through full underwriting and submitted blood and urine samples.

For those that do not meet the criteria for accelerated underwriting, you may be asked for an attending physician's report and possibly even have to undergo the paramedical exam.

The $1 million coverage limit is much higher than all the other choices out there. So, if you are in great health and need more than $500,000 in life insurance, Principal may be a good fit.

For more info, see the write-up on Principal No-Exam insurance.

Sample No-Exam Term Life Quotes - Principal

43-year-old male at Preferred health class - pricing per month

| Coverage Amount | 10 year | 20 Year | 30 year |

|---|---|---|---|

| $250,000 | $20.13 | $29.84 | $48.64 |

| $500,000 | $33.69 | $53.11 | $90.72 |

| $1,000,000 | $55.68 | $96.52 | $169.05 |

36-year-old female at Preferred health class - pricing per month

| Coverage Amount | 10 year | 20 Year | 30 year |

|---|---|---|---|

| $250,000 | $13.31 | $17.01 | $23.94 |

| $500,000 | $20.05 | $27.46 | $41.33 |

| $1,000,000 | $28.77 | $45.08 | $74.91 |

Legal & General America (Banner Life)

Advantages:

Disadvantages:

Those aged 40 or younger in good health and without bad habits may qualify for a coverage of up to $2 million. If you’re older with pre-existing conditions and an unhealthy lifestyle, the insurance company is likely to ask you to take a medical exam.

With A+ AM Bet Rating, you don’t need to worry about the company's financial standing. As one of the largest insurance companies, Legal & General has very few complaints and offers affordable insurance policies with a number of riders (e.g., accelerated death benefit).

Transamerica - Trendsetter LB

Advantages:

Disadvantages:

Transamerica has been around since 1928 and is on very strong financial footing, reflected in their excellent A+ confidence from A.M. Best. In terms of their no-medical offer, most reading this can probably do better.

It does excel in the living benefits. You'll get some standard ones with the policy, and they have even more options (at a cost) to customize things further to meet your needs.

$250k is a bit low these days in terms of maximum death benefits, but if you don't need high coverage and like the extras, it may be worth considering.

For more info, read our Transamerica no-exam policy review.

Sample No-Exam Term Life Insurance Rates - Transamerica

43-year-old male at Standard health class - pricing per month

| Coverage Amount | 10 year | 20 Year | 30 year |

|---|---|---|---|

| $50,000 | $17.12 | $21.85 | $28.86 |

| $150,000 | $30.20 | $44.13 | $66.19 |

| $250,000 | $48.59 | $71.82 | $107.89 |

39-year-old female at Standard health class - pricing per month

| Coverage Amount | 10 year | 20 Year | 30 year |

|---|---|---|---|

| $50,000 | $12.09 | $16.26 | $21.04 |

| $150,000 | $23.10 | $30.97 | $38.45 |

| $250,000 | $36.77 | $49.88 | $62.67 |

American Amicable - Term Life Made Simple

Advantages:

Disadvantages:

The "Term Made Simple" policy by American Amicable strives to be just that and is a popular choice for our clients. They are an "A" rated carrier with rating agency A.M. Best and one of the first companies to sell life insurance (1910).

Up to $400,000 in face amount is available without having to take a medical exam or submit any blood work. American Amicable includes several riders at the base premium price with the choice of many others to meet your needs. A nicely rounded life insurance policy.

For more info, see our detailed American Amicable no-exam review.

Sample No-Exam Term Life Insurance Quotes - American Amicable

42-year-old male at Standard health class - pricing per month

| Coverage Amount | 10 year | 20 Year | 30 year |

|---|---|---|---|

| $100,000 | $21.96 | $30.24 | $40.59 |

| $250,000 | $43.65 | $65.25 | $90.23 |

| $400,000 | $66.06 | $100.62 | $140.58 |

38-year-old female at Standard health class - pricing per month

| Coverage Amount | 10 year | 20 Year | 30 year |

|---|---|---|---|

| $100,000 | $15.93 | $18.72 | $25.02 |

| $250,000 | $27.45 | $37.13 | $52.20 |

| $400,000 | $40.14 | $55.62 | $79.74 |

Assurity - Lifescape Non-Med Term 350

Advantages:

Disadvantages:

Assurity is a solid option, but it's only right for certain people, such as those in excellent health and possibly smokers. The rates at the lower health classes are among some of the most expensive.

No concerns on the financial front as an A.M. Best "A-" rated insurer. Assurity does have the ability to place some tougher cases that other insurance carriers won't approve without an exam.

For more info, take a look at our Assurity No-Exam Review.

Sample No-Medical Exam Premiums - Assurity

40-year-old male at Standard Plus health class – pricing per month

| Coverage Amount | 10 year | 15 year | 20 Year | 30 year |

|---|---|---|---|---|

| $100,000 | $27.93 | $32.89 | $39.41 | $51.76 |

| $200,000 | $49.76 | $59.68 | $72.73 | $97.44 |

| $300,000 | $71.60 | $86.48 | $106.05 | $143.11 |

35-year-old female at Standard Plus health class – pricing per month

| Coverage Amount | 10 year | 15 year | 20 Year | 30 year |

|---|---|---|---|---|

| $100,000 | $15.40 | $17.31 | $20.10 | $26.53 |

| $200,000 | $24.71 | $28.54 | $34.10 | $46.98 |

| $300,000 | $34.02 | $39.76 | $48.11 | $67.43 |

Fidelity Life - Rapid Decision Express

Advantages:

Disadvantages:

Fidelity really excels in the technology game when it comes to underwriting. You will have a decision within 48 hours. They will check your driving record, Medical Information Bureau, and prescription (Rx) history. All done within minutes. Never any doctors’ records review, exam, blood, or urine tests of any kind.

Very strong receiving an "A" rating from A.M. Best, Fidelity is a well-known name in the insurance industry. We don't place a ton of clients with them, but when it's right, it's right, and certainly is one to consider.

For a deeper dive see our Fidelity No-Exam Review.

Sample Term Life Quotes with No-Exam - Fidelity

40-year-old male at Standard health class - pricing per month

| Coverage Amount | 10 year | 20 Year | 30 year |

|---|---|---|---|

| $50,000 | $21.92 | $22.45 | $34.23 |

| $100,000 | $25.32 | $35.32 | $60.64 |

| $250,000 | $52.20 | $77.21 | $140.51 |

35-year-old female at Standard health class - pricing per month

| Coverage Amount | 10 year | 20 Year | 30 year |

|---|---|---|---|

| $50,000 | $21.62 | $22.14 | $23.92 |

| $100,000 | $19.31 | $23.40 | $32.45 |

| $250,000 | $37.19 | $47.42 | $70.04 |

SBLI - Guaranteed Level Premium Term

Advantages:

Disadvantages:

SBLI uses all health classes without an exam. They do it at the same rates as fully underwritten insurance, so it's a great company to consider if you want to forgo getting pricked.

By offering all health levels, you can take advantage of your good health and save money. On the other side, they'll approve people with some health concerns, even without needing the examination.

The underwriting process can be very quick for some as they strive to do it all electronically. In this case, approvals can come back on the same day. For those applicants that require medical records review, the process can take up to 30 days for an answer.

With great pricing, a strongly rated company, and all health classes available, SBLI is a major player right now for no exam policies.

For more info, see our detailed SBLI no medical exam review.

Sample No Physical Exam Rates - SBLI

42-year-old male at Standard Plus health class - pricing per month

| Coverage Amount | 10 year | 20 Year | 30 year |

|---|---|---|---|

| $150,000 | $19.43 | $29.71 | $45.88 |

| $350,000 | $33.03 | $48.89 | $82.14 |

| $500,000 | $39.88 | $65.32 | $111.03 |

39-year-old female at Standard Plus health class - pricing per month

| Coverage Amount | 10 year | 20 Year | 30 year |

|---|---|---|---|

| $150,000 | $15.05 | $21.62 | $30.12 |

| $350,000 | $24.40 | $34.79 | $50.03 |

| $500,000 | $26.88 | $42.92 | $66.39 |

Mutual of Omaha - Term Life Express

Advantages:

Disadvantages:

Mutual of Omaha is one of the most well-known names when it comes to life insurance and receives the 2nd highest financial stability rating possible (A+) from A.M Best agency. It's no surprise they possess a solid product for those wanting to skip the exam. They even offer smaller whole-life insurance policies that don't require it.

Term Life Express includes some really good living benefits you don't see elsewhere, such as the Residential Damage Rider, which pays you out on damage to your home.

The cost of premiums is a little higher than others, but depending on needs, it can be a good value when you look at everything you are getting for your money.

Similar to many other non-med carriers, they do not give access to higher health levels unless you take a medical examination. If you are in excellent health, this probably is not your best option.

For more info, see our Mutual of Omaha No-Exam Review.

Sample No-Exam Term Life Quotes - Mutual of Omaha

40-year-old male at Standard health class - pricing per month

| Coverage Amount | 10 year | 20 Year | 30 year |

|---|---|---|---|

| $100,000 | $28.57 | $34.89 | $45.30 |

| $200,000 | $51.80 | $64.44 | $85.26 |

| $300,000 | $75.03 | $93.98 | $125.22 |

35-year-old female at Standard health class - pricing per month

| Coverage Amount | 10 year | 20 Year | 30 year |

|---|---|---|---|

| $100,000 | $18.51 | $23.14 | $29.73 |

| $200,000 | $31.68 | $40.94 | $54.11 |

| $300,000 | $44.86 | $58.74 | $78.50 |

Carriers Removed From Best No Exam Life Insurance In 2026 Due To Product Changes

Nassau RE

Advantages:

Disadvantages:

This product packs quite a bit of value for the price. The living benefits are as good or better than just about every other non-medical insurance carrier out there. If these kick in, the policyholder can take up to 95% of the face amount, which is really high.

Formerly known as Phoenix life insurance company, Nassau uses an express product that is approved within 24 hours, and those that don't qualify may need their medical records reviewed but still won't need to submit any blood or urine samples.

This can also be a good one for those with some health concerns that don't want to go through with a paramedical exam. Nassau will still approve many cases at sub-standard rates, although you'll pay more.

Nassau allows for conversion to permanent insurance within the first 5-10 years of policy issuance, depending on the term length chosen.

Sample No Medical Exam Premiums - Nassau Life Insurance

33-year-old male at Standard health class - pricing per month

| Coverage Amount | 10 year | 20 Year | 30 year |

|---|---|---|---|

| $100,000 | $15.97 | $17.69 | $22.44 |

| $250,000 | $30.59 | $34.91 | $46.77 |

| $500,000 | $54.97 | $63.60 | $87.34 |

33-year-old female at Standard health class - pricing per month

| Coverage Amount | 10 year | 20 Year | 30 year |

|---|---|---|---|

| $100,000 | $14.93 | $16.40 | $19.50 |

| $250,000 | $28.00 | $31.67 | $39.44 |

| $500,000 | $49.80 | $57.13 | $72.66 |

American National - Signature Term Express

Advantages:

Disadvantages:

American National is another financially strong insurance company playing in the non-med game. They have an "A" grade from A.M. Best. Their underwriting is known for approving some tougher cases with medical issues. Although this may require a little longer, but usually worth the wait.

ANICO includes what are known as "living benefits" automatically. These allow for the acceleration of the death payout in cases of certain illnesses. They do this while still staying very competitively priced. American National is definitely high on the list of no-exam life insurance companies.

In addition to the no exam term product, they have a whole life policy for up to $150,000 that does not require a physical examination either.

For more info, see our detailed American National no medical exam review.

Sample No-Medical Term Life Premiums - American National

40-year-old male at Standard health class - pricing per month

| Coverage Amount | 10 year | 20 Year | 30 year |

|---|---|---|---|

| $50,000 | $14.21 | $17.02 | $20.61 |

| $100,000 | $14.26 | $19.35 | $28.94 |

| $200,000 | $23.33 | $33.52 | $52.70 |

35-year-old female at Standard health class - pricing per month

| Coverage Amount | 10 year | 20 Year | 30 year |

|---|---|---|---|

| $50,000 | $10.37 | $12.74 | $16.03 |

| $100,000 | $10.80 | $14.43 | $18.14 |

| $200,000 | $16.42 | $23.67 | $31.10 |

Sagicor - Sage Term

Advantages:

Disadvantages:

Sagicor is a major player in the non-med policy market. With an A.M. Best grade of (A-) and quick approval times, it's no wonder it continues to be popular among our clients.

The underwriting process is fully digital, and they'll never ask to see your medical records. Most approvals are done within a few minutes. Hard to find anything faster.

Policy face amounts go up as high as $1,000,000, which is among the highest for no-exam life insurance. Another great thing is they are one of the few companies that will give you a Preferred health class. This makes them definitely one to consider if you are in great health, as you'll save a ton. On the flip side, they will take substandard business cases with some health challenges.

Sagicor also offers their Sage NLUL (Index Universal Life) product, and this, too, can be issued without the need for a medical exam. This is an index universal life insurance policy.

For more info, see our detailed Sagicor no-exam review.

Sample No-Exam Premiums - Sagicor (No longer offering term options)

40-year-old male at Preferred health class - pricing per month

| Coverage Amount | 10 year | 15 Year | 20 year |

|---|---|---|---|

| $100,000 | $15.15 | $18.03 | $21.64 |

| $300,000 | $31.91 | $38.98 | $48.74 |

| $500,000 | $48.98 | $60.77 | $77.03 |

35-year-old female at Preferred health class - pricing per month

| Coverage Amount | 10 year | 15 Year | 20 year |

|---|---|---|---|

| $100,000 | $11.44 | $12.74 | $15.01 |

| $300,000 | $21.43 | $23.10 | $30.21 |

| $500,000 | $31.51 | $34.30 | $46.15 |

How Does the No Medical Process Work?

The typical life insurance process involves a paramedical professional or "paramed" coming out to your home to perform a physical examination.

While there, they measure your blood pressure levels, check your cholesterol, record your height and weight, and collect a blood and urine sample.

There will also be detailed health questions about your medical history and any medications and supplements you take. This information will be sent to the underwriting department, which will compare it against their company guidelines.

You may also need to submit information about your employer, income, and salary to help determine just how much life insurance coverage you qualify for.

But without the exam...

Yes, there is still underwriting, but it's faster and easier. This is why these policies are often called "simplified issues".

They will run some electronic checks on your driving record, pharmacy (Rx) report, and the MIB, which is a consumer reporting agency that insurance companies share medical information with.

Who Should Buy Non-Med Life Policies?

The big three we see most often are:

1) Time - We are all busy, and finding time to have the paramed out to do it just isn't convenient.

2) Fear of needles or blood - This is real, and it's a major reason people delay putting a life insurance policy in place.

3) Need the coverage in force fast - With most life insurance companies, the no-exam route will be much quicker.

The important reason people don't know about - You haven't been to the doctor in some time. If it's been more than 2 years, your vital levels, like cholesterol, may have changed slightly for the worse, which means you'll pay more.

We usually advise our clients to get a no-exam policy in place first.

If you like, you can always go look for a fully underwritten policy afterward if you are willing to submit to the exam to try and save a few more bucks.

If you do it the other way around, there is no going back. Those lab results are now part of your medical files and will be seen, even by non-medical underwriting.

Frequently Asked Questions

What is the oldest age to apply for a no-exam policy?

New York Life and Nassau Insurance companies will both accept applications up to age 80. Final Expense policies can go as high as 89.

What is the highest death benefit available for a non-med policy?

Principal and John Hancock both offer 1 million without taking an exam if you are in excellent health and qualify for the Preferred rate class. Sagicor, SBLI, and Nassau all go up to 500k at lower health classes.

Can I combine no-exam policies from different companies?

Yes, policies from different companies can be stacked to get a higher coverage amount. Separate applications and underwriting reviews will be required.

Do I have to disclose a risky hobby or job on the application?

Only if they ask about it. Discuss your specific situation with an independent agent so you apply at the right company.

Is no medical exam life insurance policy available in my state?

Yes, there are no-exam policies offered in all 50 states and the District of Columbia. Certain insurance companies may not do business in some states. New York, in particular, has fewer exam options.

How much more does it cost for a no medical exam policy?

Anywhere from 0% to 43% and higher. We will typically provide our clients with both options so they can decide. For more info, see our detailed cost comparison.

Is Guaranteed Issue life insurance really guaranteed?

Yes. As long as you fall in the age range, everyone is approved. The high cost, low coverage amount, and waiting periods for death benefits allow this to be possible. This should always be a last resort after you have worked with your independent broker to discuss options.

Can whole-life insurance be purchased without taking a medical exam?

Yes. Many companies now offer small whole-life policies that do not require a medical exam. The above guide focuses mainly on term life no exam policies, but many of these same insurers have whole life options too. Contact us to discuss this if interested.

Many no-exam term policies can also offer the right to convert to a permanent product down the road.

Are there still underwriting and medical questions for no-exam policies?

Yes. The other parts of the underwriting process are very important with no-exam policies since the company can't rely on the lab results. An in-depth explanation, including exactly what is checked, can be seen in our earlier section on the no-exam underwriting process.

What is the fastest no-exam coverage available?

Penn Mutual offers immediate decisions on certain products, and SimplyTerm from Prudential is usually done in 2 days. Sagicor and Fidelity can approve same day and usually within 72 hours. Metlife can do approvals in 1-2 days.

What health classes are available on policies that don't require a medical exam?

Many insurance carriers will only offer up to the Standard health class on their no-exam products. Penn Mutual and Banner Life will offer Preferred rate classes for those in excellent health. Principal and Prudential will ONLY offer Preferred.

Can I do the no medical exam insurance application myself?

Most of the companies require an agent to submit the application with you. This is for your protection and does not cost you anything. Life insurance rates are fixed by law, so nothing is saved by applying directly to the insurance carrier, even if they allow it.

How long does no medical exam life insurance last?

The duration of no-exam life insurance policies will depend on whether your policy is permanent or not. In case it is not, your no-exam life insurance will last up to a predetermined age.

Can I borrow money from a no-exam life insurance policy?

You may be able to borrow money if you have permanent no medical exam life insurance. The amount you can borrow will also depend on the accumulated cash value and other factors noted in your policy. In case of inability to repay back, the insurance company will not pay the full death benefit.

Need Help?

If you haven't noticed by now, we are pretty passionate about no medical exam life insurance. We believe it will continue to grow and improve to the point where it's the standard.

If you'd like to have a no-pressure chat about options for protecting your loved ones, check out some quotes on our site and enter your information so we can get in touch with you soon.