MetLife Life Insurance – A Comprehensive Review

What if you could get pre-approved by one of the world’s largest insurance providers?

Certainly MetLife, the nearly 150-year old insurance carrier that Fortune magazine once called the World’s Most Admired Company is well-positioned to offer you the best life insurance policy available in today’s market, right?

Not necessarily.

The truth is that life insurance is not a one-size-fits-all product, and while MetLife’s policies are a fantastic choice for some people, there is no guarantee that their policies are right for you.

In order to find out, you need to study MetLife’s policies, its track record, and its history of payouts. This information, along with the data we’re going to provide below, is critical to determining whether MetLife really is the right life insurance provider for you.

Beginning with an overview of the company, and moving on to a comprehensive step-by-step walkthrough of its life insurance products, we’ll help you determine whether MetLife is the right insurer for you below.

Introducing MetLife

Founded in 1868, MetLife is one of the oldest, largest providers of insurance, annuity, and employee benefits programs in the world. With $900 billion in total assets, it has earned the 42nd slot on the Fortune 500. You may seem them referred to as Metropolitan Life.

Although it carries a wide-ranging catalog of insurance products, we’re only going to focus on MetLife’s life insurance policies. Be aware that these policies may be sold under the name Brighthouse – a spin-off company to which MetLife has entrusted its retail insurance products.

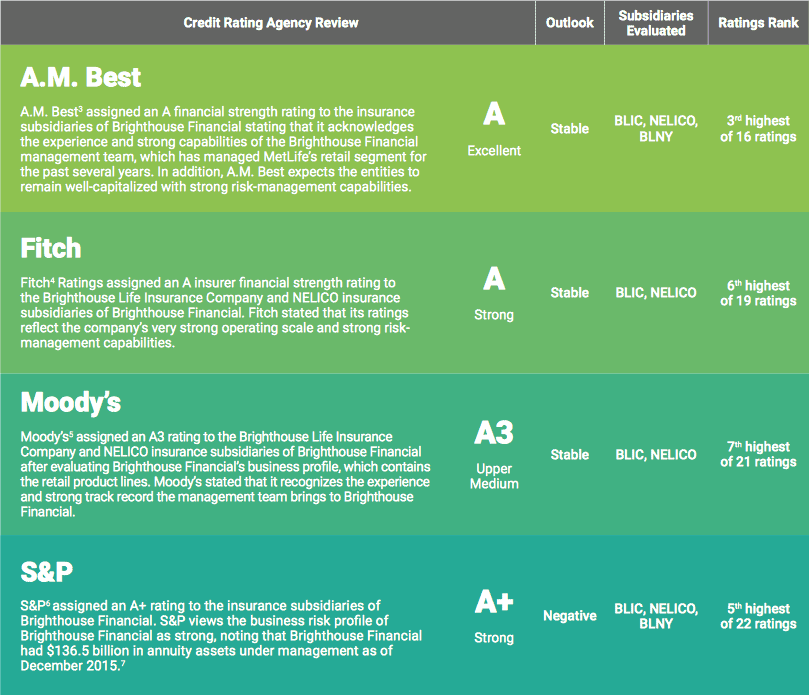

When dealing with a company the size of MetLife, it helps to be as specific as possible. In order to zero in on the company’s eligibility as a life insurance provider, we need to look at the credit rating and solvency of Brighthouse Financial.

- A.M. Best, the most important rating agency for insurance providers, gives Brighthouse an A – the third-highest of its 16 ratings categories.

- Fitch also granted an A-rating to the retail insurance provider, giving it the 6th highest rank within its 19 places.

- Moody’s assigned an A3 rating, which underscores the stability of the company. This is the 7th highest rating out of 21.

- Standard & Poor assigned an A+ to Brighthouse, the 5th highest rating out of 22.

What these ratings mean is that the company is on solid ground financially. It has enough assets – and those assets have enough liquidity – to pay out life insurance claims without having cash flow issues. MetLife must strictly observe these financial solvency standards to remain in regulators’ good graces. Financial strength is definitely a box MetLife checks and does well.

MetLife Life Insurance Review

As mentioned above, MetLife offers a dizzying array of insurance products and coverage options. In order to identify whether it could be your first-choice life insurance provider, we will analyze some of its most popular life insurance products.

MetLife Term Life Insurance

MetLife’s term-issue life insurance wins points for its simplicity. You can get a policy with a death benefit of less than $100,000 without having to undergo a medical exam. This represents an easy way to secure a minimal amount of coverage for a set term – policies typically stipulate terms between 10 and 30 years.

MetLife’s simplified term life insurance is ideal for people who need to get coverage fast – such as those undergoing divorce. In this case, it may be in the policyholder’s best interest to skip the exam and get a signed policy agreement so that alimony can be protected.

However, considering the low face value MetLife’s no-exam term life insurance policy covers, it may not represent the kind of comprehensive life insurance coverage that you need. For higher face values (death benefit), you’ll want to see a doctor and have some concrete medical data on-hand – in many cases, this can result in less expensive coverage.

For instance, consider the following example rates – these would apply to a 35-year old male non-smoker eligible for Preferred Plus term life insurance rates:

(Rates are subject to change and must be qualified for.)

Permanent Life Insurance

If you are interested in locking in a life insurance policy for the rest of your life, a MetLife permanent policy may be the right choice for you. Permanent coverage is an ideal solution for business succession agreements in which several stakeholders wish to endow their business partners with their respective stakes in the business – transferring their part into cash for their families in the process. In this case, the fact that permanent life insurance accrues value over time makes it preferable to a term policy – especially over long periods of time.

MetLife’s size and reputation are definite advantages when considering taking out permanent life insurance. MetLife offers face amounts that range from $100,000 to $1 million, and certain special qualifiers that might make your deal more valuable.

In particular, the Enhanced Rate Plus Program allows you to take out a permanent life insurance plan without requiring a medical exam. Instead, all you need to do is fill out a web application form and participate in a telephone interview with a MetLife underwriter.

Whole Life Insurance

Whole life insurance differs from term in four important ways. First, it guarantees benefits upon death. Second, it guarantees a fixed premium for the life of the policy. Third, it is guaranteed to accrue value over time. Fourth, if you are looking for cheap life insurance, whole life is not for you.

MetLife pays dividends on whole life insurance policies, which lets beneficiaries purchase additional life insurance, receive payouts as cash, or reduce premium payments.

As with many of its other life insurance policies, MetLife offers a low-cost version of its whole life insurance policies that doesn’t require a medical examination. This is called Guaranteed Acceptance Whole Life Insurance, and may be a valuable tool for individuals who wish to gain minimal coverage at a low cost.

Guaranteed Acceptance Whole Life insurance generally covers between $2,000 and $20,000 – a small fraction of what a good term policy would cover. However, there are situations when this is ideal. For instance, MetLife will not decline these policies for individuals between the ages of 50 and 75, even for health reasons.

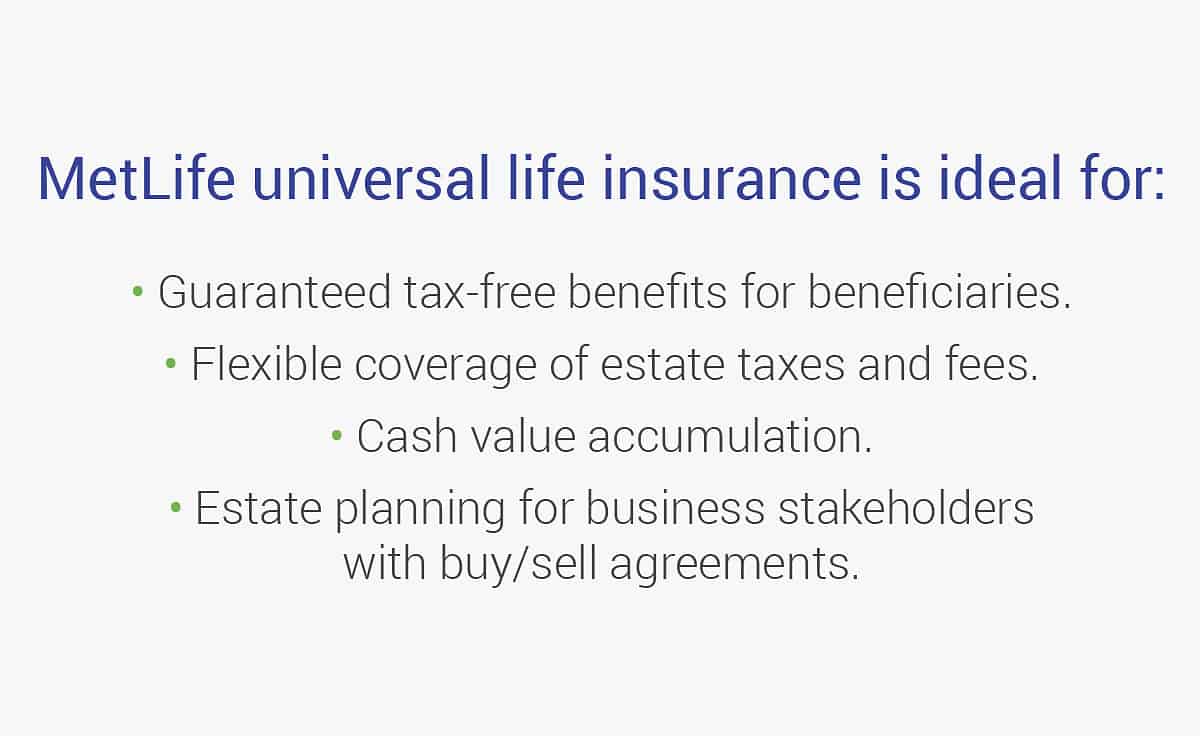

Universal Life Insurance

Universal life insurance is similar to Whole Life, but gives you greater control over how the policy’s cash value accumulation is invested. In particular, the policyholders can use the cash value of the policy to supplement retirement portfolios. They also have additional options such as survivorship – combined policies that only pay out when both the principal and the principal’s spouse dies, decreasing the cost of insurance and leaving more to heirs.

The reason why MetLife’s universal policies can be so flexible is that they are age-specific, not term-specific. This means that you specify the age until which you wish to be covered and work out what kind of premium payments suit your needs best. At any point after that, you are still free to alter your premium payments, withdraw cash from your cash value fund, or change the face value of your policy.

MetLife universal life insurance can be very useful for people who expect to live beyond the age of 80. This is because most of the company’s term life insurance policies do not extend beyond that age even in the best of circumstances, while a Universal policy easily can.

This is the type of insurance ideally suited for a buy/sell agreement as mentioned above. It may also offer advantages for covering estate taxes, fees, and outstanding medical bills, or even for forming a charitable trust.

Final Expense Life Insurance

MetLife’s Final Expense policy offers guaranteed coverage without requiring a medical exam or even health questions. This type of insurance policy covers funeral expenses on a two-year graded benefit scale – MetLife will not pay out the full-face amount of the policy until it has been active for two years.

Since MetLife’s Final Expense insurance policy bridges the gap between life insurance and prepaid funeral plans, it is best-suited to individuals who are terminally ill or in hospice care. Otherwise, you can probably get a better deal through a small whole life insurance policy. Also, if the insured person is unlikely to live out two years from the signing of the policy, another provider may offer a better insurance product.

Riders

Metlife offers a wide variety of life insurance riders and options to customize your policy depending on your individual needs. The numerous options are outside the scope of this article but a knowledgeable insurance agent can walk you through the costs and benefits.

Who Signs Up for MetLife Life Insurance?

Most insurance companies have one or more niches – segments of the population they serve particularly well – and MetLife is no different. Some of the niches in which MetLife’s insurance products outperform the competition include:

- Diabetics. MetLife excels at insuring clients who suffer from Type 1 and Type 2 diabetes.

- Active Military Personnel. MetLife caters to the needs of active military personnel and markets particularly aggressively towards that target market.

- Seniors with Blood Pressure Issues. MetLife performs better than other insurance providers when it comes to older people with blood pressure issues. For instance, most providers wouldn’t put a senior with a blood pressure reading of 140/85 in their Elite Plus rate class – but MetLife does. Even seniors with higher blood pressure readings of 170/90 still qualify for standard rates.

- Marijuana Users. MetLife is generally lenient when it comes to marijuana use. At least, it does not automatically offer tobacco-user rates to marijuana users, which is more than can be said of many other insurers.

Importantly, these facts don’t automatically mean that a MetLife policy is going to be right for you. They only suggest that people who fall into the above-mentioned categories have generally had positive experiences when taking out a policy or filing a MetLife life insurance claim.

Compare MetLife to Other Providers

In order to truly determine whether MetLife is the provider you need, you need to rely on an independent life insurance expert and broker. Only a reputable broker has the experience to identify the advantages and disadvantages of life insurance policies based on the provider issuing the policy.

Fortunately, we can help you find out if MetLife is the right provider for your life insurance policy and compare rates from them alongside more than 60 other life insurance providers. To start, simply fill out the form below and we’ll get to work comparing insurance rates on your behalf.

Simple Life Insure is an experienced, reputable broker that aggregates insurance policies from more than 60 different providers in order to find the ideal policy for each individual. Fill out our standard data form and get free term life insurance quotes today!